Phase One – Planning

1. Build a Budget

Setting a budget will give you the foundation to create a solid financial plan. In order to build a budget, you need to understand what your current situation is by looking at where you bring in money versus where you spend it. To understand the flexibility you have with your budget, you should know the difference between Fixed and Variable costs.

Fixed – Expenses that do not change on a regular basis or cannot be easily adjusted. Examples: rent, insurance, utilities, student loans, etc.

Variable – Expenses that are flexible or easily modified. Examples: food & dining, health & fitness, travel & leisure, shopping, etc.

2. Define a Goals Based Strategy

Now that you have the movements within your financial ecosystem defined, you can begin forming goals and make a plan for how to achieve them. As you begin this process, ask yourself what kind of things or experiences are important to me? Education? Buying a home? Travel? What is the timeline for achieving these?

Short Term: 1-3 Years | Intermediate Term: 4-7 Years | Long Term: 7+ Years

It is important to remember that you can always reassess your goals if needed. Life can often change them for you, and you should try to recognize when a shift in priority takes place. Your dream of traveling the world for a year might be put on hold if children become part of your immediate future.

3. Plan for your Retirement

Keeping in mind what you want out of life, it is critical to recognize which unique tools for retirement can empower you to save for that bright future.

The best and most common tools offered to us by Uncle Sam, and in some cases our employer, is the traditional IRA, Roth IRA, and 401(k).

Roth IRA: Allows you to pay taxes on your contribution now in favor of tax-free growth.

Traditional IRA: Allows you to contribute now for an immediate tax deduction in favor of tax-deferred growth.

401(k): Can be treated as Roth or IRA depending on what your employer offers and your election. Check if your employer matches contributions and try to take full advantage if they do. It’s as close to a free lunch as you can get!

Phase Two – Implementing

Implementing your plan can seem daunting. Picture a mountain. From a distance, it is a steady climb, but as you get closer many different paths emerge to get to the top. Each one has its own set of challenges, unique ups and downs, but the goal is always the peak. That mountain is, hopefully, a picture of what your nest egg looks like over time. Now it’s time to take steps toward that goal at the top.

4. Understanding Risk and Asset Class Diversification

Understanding risk helps you navigate the best path to achieve the goals you set in the planning phase. The biggest risk we face as individual investors is falling short of our goals, not volatility (price swings) in the market. We manage risk primarily through investing across asset classes. Meaning what area of the financial markets you invest in.

We can change the risk of our portfolio through adjusting the weights and exposures to different asset classes and securities we hold, what we call diversification. Keep in mind that your portfolio allocation should match the time horizon of your goals. Money needed for a short-term goal should not be held in volatile investments and long-term goals should not pair with dollars in ultra-conservative investments.

5. Stock Options & Restricted Stock Units (RSU’s)

Stock Options: Represent a right to purchase company stock at a certain price.

RSU’s: Grant ownership in the company.

This is not relevant for everyone, but we commonly see them as additional methods of compensation. You should consider discussing them with your financial and tax advisors before entering into an agreement with your company. It is worth having them analyze the specifics of the agreement and ask if you qualify for the 83(b) election. Be aware of the potential risks of letting these become too much of your portfolio since they rely on the performance and market outlook of a single company to drive returns.

83(b) Election: Gives you the option to pay ordinary income tax on the fair market value at the time of receipt and capital gains rates at the time of sale.

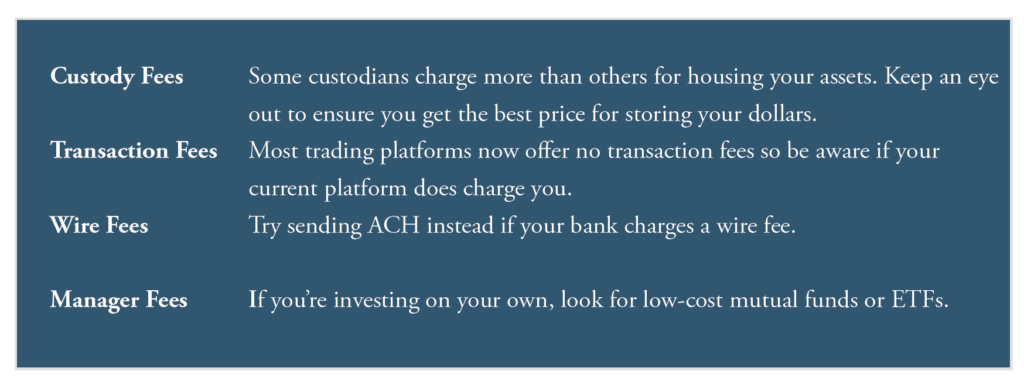

6. Know Your Costs

Costs can be thought of as the weight you decide to carry with you towards the top. Over time, even small fees can slow you down. It is important to look at how much you pay in fees and try to mitigate them when possible. Similar to budgeting, know what they are and where they come from to determine if they can be avoided. The ones we most commonly see are:

Phase Three – Maintaining

Relationships, valued possessions, and health, all require regular maintenance to keep your life running smoothly; your finances are no different. Exploring the most efficient ways to navigate your financial journey will help you to achieve your definition of success.

7. Manage Your Portfolio and Ignore the Noise

There is no sense in creating a plan to reach your goals if you do not stick to it. It is imperative you follow the course you set for yourself and focus on your own path. That means not letting day to day swings in markets or that trending Twitter recommendation drive your decision making.

This is where knowing your risk tolerance and keeping an unemotional systematic approach to your investing strategy is key to avoid veering from your plan. Remember that to achieve your goals, you must think about the big picture and buckle up for the ride ahead.

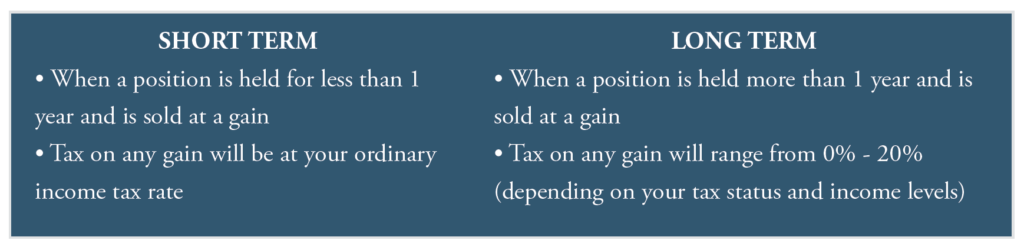

8. Navigate Capital Gain Exposure

We have all heard the only guarantees in life are death and taxes. Luckily, you can take steps to defer the inevitable and make them a little less painful when the time comes to pay up. No, we are not talking about cryogenic freezing.

We are talking about strategically realizing capital gains and losses generated from your portfolio. A capital gain/(loss) is the difference between your tax cost basis or purchase price and the price at which you sell an asset. Here the patient investor wins by avoiding selling short-term gains in favor of long-term capital gains rates. Strategically pairing losses with gains also helps to avoid a heavy tax burden come time to file.

9. Identify and Maximize Tax Deductions

Itemizing your deductions could help you save money when you file. It can be thought like creating your own itemized receipt at from a store or restaurant. You can claim expenses paid throughout the year to exempt you from having to pay taxes on money you needed to live. In some cases, this may add up to more than what is granted to you when you take the standard deduction.

10. What You Need to Know About Charitable Giving

For those looking to make an impact, charitable planning can be a fulfilling experience. You can also deduct those donations on your tax return by itemizing.

Regardless of the goal, you have a couple tools at your disposal to align with what you want. Donor Advised Funds (DAF’s) and Private Foundations both offer a way to provide for the causes you feel strongly about while granting you a tax deduction on the dollars you contribute today. Both will allow money contributed to grow tax free while they live in those entities. DAF’s offer a simple and cost-effective way to donate to public charities while foundations require higher maintenance costs for a higher degree of control and creativity for what those funds get spent on.

In case you missed it, our FuturePath committee hosted a webinar on the 10 Financial Planning Fundamentals to Navigate your Financial Future. We invited panelists from our experts in tax, client advisory, and research team to go over the core concepts we use and teach every day to empower thoughtful management of our clients’ financial health. You can access the video and handbook to learn more on how to take control of your finances.

If you have any questions, would like to discuss financial planning fundamentals, or how you can take control of your finances, please contact us.

Please see the PDF version of this article for important disclosures.