Who and When to Enroll?

If you are 65 and receiving Social Security, you likely have been enrolled automatically for Medicare Parts A & B. However, if you continued to work, took early retirement, or deferred receiving Social Security benefits, you may have to take active steps to enroll in Medicare once you turn 65.

Enrollment in Medicare takes place during a seven-month period based on your birthday, referred to as the Initial Enrollment Period. The enrollment clock begins 3 months before the month you turn 65, includes the month you turn 65, and ends 3 months after the month of your birthday. For example, if you turn 65 in June, your Initial Enrollment Period begins in March and ends in September. If you enroll during the initial seven-month window, you avoid penalties and gaps in coverage.

If you are over 65 and not yet on Medicare because you are working and covered by a group health plan or covered through a group plan provided by a spouse who continues to work, it is imperative you remember to enroll in Medicare Parts A & B once the employment-related coverage ceases.

Need to sign up for Medicare? It is now easily accomplished online and will take about ten minutes of your time.

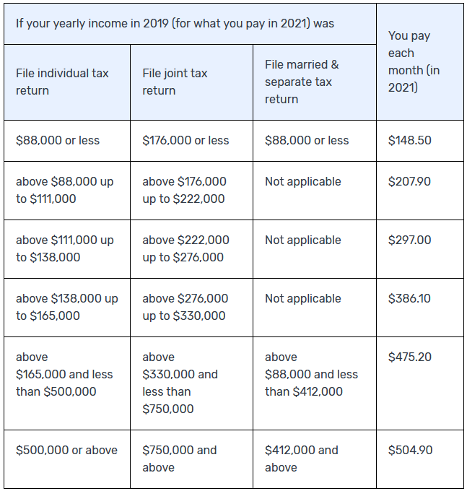

Current Cost of Medicare Part A & B

Medicare Part A covers hospital-related services, and for individuals or spouses who have paid Medicare taxes while working, Medicare Part A is premium-free.

Medicare Part B covers physician-related services and the current monthly premium paid is related to your taxable income as follows:

Importance of Meeting the Medicare Enrollment Deadline

Avoiding Late Enrollment Penalty

If you do not sign up for Part B when first eligible, a 10% penalty is assessed to the Medicare Part B premium for each 12-month period in which you were eligible for Part B but were not enrolled. For example, Bob’s Initial Enrollment Period ended in September 2018 but he did not sign up for Part B until March 2021, which means a total of 30 months passed from the end of Bob’s Initial Enrollment Period. In this scenario, a 10% penalty is assessed for each 12-month period without Medicare Part B coverage, so Bob would pay a 20% penalty on the amount of his Part B premium. Keep in mind that this is not a one-time penalty: Bob will pay the 20% penalty on his premium for the entire time he carries Medicare Part B.

Avoiding a Gap in Coverage

While the late enrollment penalty can be costly, a gap in coverage can be financially devastating. If you miss the Initial Medicare Enrollment Period, the next opportunity to enroll is during Medicare’s General Enrollment Period which runs from January 1 to March 31 each year. However, it is important to note the coverage would not begin until July 1st. Because insurance carriers do not offer individual health insurance coverage for those over the age of 65, a coverage gap would occur if you were not covered by a qualifying group health insurance plan thereby self-insuring all medical claims until coverage commences.

Is There Ever a Time to Delay Medicare Part B Enrollment?

Yes! There are scenarios when a delay in signing up for Part B is appropriate and would not include the risk of late penalties, for example:

- You are covered by a group health insurance plan from your employer who has 20 or more employees, and you are still working, or

- You are covered by your spouse’s group insurance plan through his/her employer with 20 or more employees and your spouse is still working.

To avoid the penalty and coverage gap pitfalls, the two key conditions are that you or your spouse must be an active employee, and the company must have 20 or more employees.

Avoid the COBRA Trap

Finally, it is important to understand that Medicare does not consider COBRA and Retiree coverage as a qualified group health insurance plan. Once a person who is 65 and is not enrolled in Medicare Part B loses an employer-sponsored health plan they qualify for a Special Enrollment Period allowing them eight months to enroll in Part B. The Special Enrollment Period clock starts on the earliest date of when you lose company-sponsored health benefits or on the last day of employment.

Meet the Medicare Enrollment Deadline: Put it on Your Calendar

Add a to-do to your calendar if you haven’t already, to ensure you meet the deadline for your enrollment.

If you have any questions or would like to discuss your options, please contact us.

Please see the PDF version of this article for important disclosures. This article was originally published by Advisor Perspectives.