Background

The EU is an economic and political union among 28 European countries (including the UK). The EU traces its roots back to 1958 when following World War II, six European countries (Belgium, Germany, France, Italy, Luxembourg and the Netherlands) sought ways to increase economic interdependence in order to boost economic growth and reduce the likelihood of future conflict. The modern EU was established decades later in 1992 when twelve European countries including the UK signed the Treaty of Maastricht, a pact that paved the way for greater economic, social and political cooperation across the continent.

The economic and social principles under which the modern EU was founded are similar to the beliefs that underpin the economic and social systems of the United States (“US”). For example, the EU has a common market that allows for the free movement of people, goods, services and capital across member countries. This type of integrated market structure appealed to a previously fragmented Europe for several reasons. First, the free movement of goods, services and capital leads to increased efficiencies (e.g. no physical checkpoints at borders) and lower costs (e.g. no tariffs on goods and services) for businesses operating within the EU. Second, allowing people to travel to where their skills are in high demand and/or where there are labor shortages, in theory, leads to lower unemployment across the common market. This is important because lower unemployment tends to improve consumer confidence and spending, two factors that drive sustainable economic growth. Allowing citizens in the EU to travel freely also helps to reduce overall fluctuation in labor costs for businesses which in turn leads to greater overall price stability, another positive for economic growth. Lastly, from a global trade perspective, many believe Europe is better off together under a single customs union because it allows the EU to leverage their collective size to negotiate more favorable trade deals with the rest of the world.

While the UK’s EU membership is similar to that of other members, it is unusual when it comes to their non-participation in the monetary union. Because the UK’s membership predated the development of the Euro, the official currency of the EU, the UK was permitted to choose whether or not to adopt the Euro. Due in part to lingering Euroscepticism, the UK elected to forego formal adoption of the Euro in order to retain their monetary independence. In layman’s terms, this means they retained their currency, the British Pound Sterling, along with the control over domestic interest rate policy. The Bank of England, the equivalent to the Federal Reserve in the US, sets interest rates and manages the money supply in the UK while monetary policy across the EU is governed by the European Central Bank.

Referendum Aftermath

Polls leading up to the June 2016 Brexit Referendum projected the UK was destined to remain in the EU. However, as we witnessed in the 2016 US presidential election, polls can be imperfect forecasting tools. When the final votes were tallied, remain supporters, pundits, and spectators were left in shock as the citizens of the UK, by the narrowest of margins, had elected to leave the EU. Shortly thereafter, UK Prime Minister David Cameron, who had campaigned vigorously for the UK to remain in the EU, announced his intention to resign.

Following UK protocol, members of parliament (“MPs”) from the conservative party (Mr. Cameron’s party) were tasked with appointing the next UK Prime Minister. This process typically entails expedited campaigns by candidates and multiple rounds of voting but in this case, a frontrunner quickly emerged. Theresa May won the election with relative ease. She won the first two rounds by significant margins and her remaining opponents withdrew ahead of the final vote.

Nearly a year after securing the prime minister nomination, Ms. May called for a general election (June 2017) in hopes of increasing the conservative party’s representation in parliament. In the UK, a general election is an opportunity for constituencies in the UK to choose their MP. While many incumbent MPs tend to retain their parliament seats through these elections, there can be turnover, particularly if the election is held amid a political event with far reaching implications (such as the Brexit referendum). While Ms. May’s intentions were to solidify her party in order to bolster her negotiating power with the EU, the exact opposite happened as the conservatives actually lost parliament seats and the labour party, the UK’s second largest political party, who mainly voted to remain in the EU, gained seats.

Three Deals, Three Zonks

Where are we now? After serving as UK Prime Minister for three years and failing to deliver a Brexit deal, Theresa May resigned from her position as UK Prime Minister, effective June 7, 2019. Ms. May resigned after she was unable to construct a proposal that appealed to both hardline, pro-Brexit UK parliament members, as well as proponents of the EU, two sides with decidedly different motivations. In short, the hardline pro-Brexit camp prefers a cleaner break while the proponents of the EU prefer that the UK remain closely aligned with the EU post-split.

Ms. May’s Brexit deals were voted on and rejected by parliament on three separate occasions. In an effort to win over hardline, conservative colleagues, her proposals included plans for the UK to withdraw from both the EU customs union and single market. Leave supporters believe that withdrawing from the customs union will allow the UK to negotiate more favorable trade deals with other countries. Some of the potential benefits they see from leaving the single market include: taking back control over immigration policy, ending annual financial payments to the EU, and regaining judicial sovereignty. Though Ms. May’s final deal was actually only a proposal outlining the terms for a transition period while the UK and EU worked towards a final separation agreement, it was still rejected by a vote of 334 to 286. This proposal ultimately came up short as hardliners viewed it as too lenient, especially on one particular issue, the treatment of the border between Northern Ireland (a UK territory) and Ireland (an EU country).

The “Irish Backstop”

The treatment of the Northern Ireland and Ireland border has been a major source of contention amongst UK politicians and between the UK and EU. Given the close relations between these two countries, primarily from an economic and business perspective, ensuring the frictionless passage of goods and people across the border (e.g. having no border checkpoints or other regulatory obstacles) has been a top priority. In addition, Northern Ireland and Ireland have a long history of conflict and violence. Many fear that restoring a physical border between these two nations would risk re-igniting tension between these regions. In an effort to avoid the physical border at all costs, Ms. May and the EU agreed to a clause referred to as the “Irish backstop”. This provision would have ensured Northern Ireland remained in the EU single market and customs union in the event the UK and Brussels were unable to reach a definitive withdrawal agreement prior the UK’s official exit. Many of the British MPs voted against Ms. May’s Brexit proposals because they saw this clause, which would be in place during the transition period—at a minimum—as a threat to the UK’s long-term sovereignty, something the leave supporters promised their constituents.

Theresa May’s Successor: Have the Stakes Changed?

Following Theresa May’s resignation, two conservative politicians – former Mayor of London Boris Johnson and Foreign Secretary Jeremy Hunt – emerged as the leading candidates to become Britain’s next prime minister. Messrs. Johnson and Hunt campaigned briefly before an official vote was held. The favorite prevailed as Mr. Johnson won the election by a margin of approximately 2:1.

Leading up to the original referendum in June 2016, Boris Johnson was one of the most prominent and outspoken leaders for the leave campaign. As such, his appointment to the prime minister post was not unexpected, particularly when his predecessor was critiqued for being “too soft” on Brexit. Mr. Johnson has been openly critical of Ms. May’s handling of the Brexit negotiations and has portrayed himself as a sterner and more capable dealmaker (sound familiar?). He has already stated publicly that the UK is prepared to leave the EU without a deal on October 31st. While it is unclear whether or not Mr. Johnson will follow through on this “threat”, most analysts and pundits agree that the odds of a hard Brexit have increased. In a July poll conducted by Reuters, economists pegged the chances of a no deal Brexit at 30%, up from 25% in June and 15% in May. Odds in the UK betting market also imply an increased probability of the UK crashing out of the EU.

How have UK Markets Responded?

Stock Market

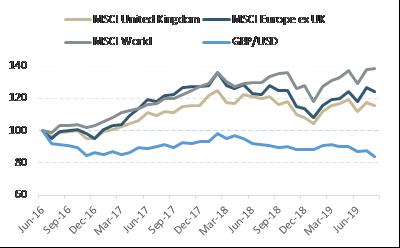

UK stocks (MSCI United Kingdom) have muddled along since June 2016. Since the referendum, in US dollar terms, the UK has underperformed the rest of Europe (MSCI Europe ex UK) and the developed world (MSCI World) by 8% and 23%, respectively. UK returns compared to the developed world would have been much stronger had it not been for the depreciation of the British Pound Sterling relative to the US dollar following Brexit.

Source — Bloomberg

Currency

Over the long term, one of the most important drivers of a currency’s valuation is economic growth expectations. From an investment standpoint, capital tends to flow to markets with solid or improving economic backdrops. When the outlook for an economy is positive, there tends to be more demand for that currency which in turn puts upward pressure on the valuation of a currency. Conversely, when there is more uncertainty and deteriorating growth expectations in a particular market, there is usually less demand for that currency and by extension downward pressure on the value of the currency.

To bring this relationship to life, foreigners generally seek to invest in markets with stable or rising currencies as it allows them to realize stable or improved returns when translating their investments back into domestic currencies. Real estate property (commercial and domestic) tends to decline in value when the economic outlook deteriorates as domestic demand is expected to be subdued in a slowing economy. On a positive note, a cheaper currency can actually be a tailwind for some UK multinational companies if their products and services become cheaper to their foreign customers.

The decline in value of the British Pound Sterling (light blue line above) has contributed to the underperformance of the UK stock market, from an unhedged US investors’ perspective. The British Pound fell initially following the 2016 referendum, a move symbolic of consensus expectations that the UK economy would likely slow/contract following the UK’s exit from the EU. Despite a rebound in 2017 amid a significant rally in global equities, particularly foreign stocks, in aggregate the British Pound has lost approximately 16% of its value versus the US dollar since June 2016.

Conclusion

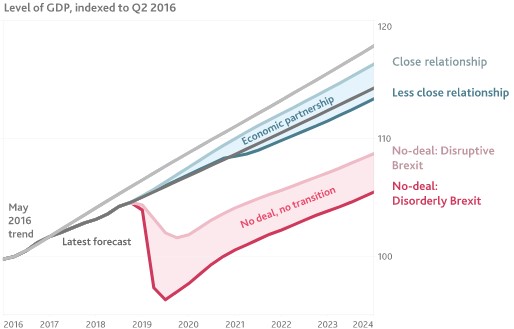

As the saying goes, the devil is in the details. A little over three years have passed since the initial referendum and the UK and the EU are still scrambling to negotiate the final terms of the UK’s exit from the EU. If the two sides fail to strike a deal prior to the October 31st deadline, the UK will leave the EU without clarity on key economic policies (e.g. trade treaties) and social issues (e.g. border control). Economists, think tanks and UK politicians agree that under this scenario, the UK is likely to slide into a recession. The graph below, published by the Bank of England, forecasts the impacts of various Brexit scenarios on the UK’s gross domestic product (“GDP”) over the next five years. A “Disorderly Brexit”, the worst case scenario outlined in the graph, assumes the UK loses access to existing trade agreements, the Bank of England enacts less accommodative monetary policy, and interest rates on sovereign debt, household loans and businesses all increase significantly. Further background on the Bank of England’s EU withdrawal scenarios can be found online at the following address:

https://www.bankofengland.co.uk/-/media/boe/files/report/2018/eu-withdrawal-scenarios-and-monetary-and-financial-stability.pdf

Over the past three and a half years, the Brexit plot has had no shortage of twists and turns. With the October deadline less than two months away, the narrative appears to be shifting yet again. Boris Johnson’s Brexit crusade was dealt a significant blow on September 2nd after a conservative parliament member’s withdrawal from the party caused the conservative party to lose its majority. His negotiating power was further weakened over the subsequent days as parliament voted to approve legislation that would give them the power to force the prime minister to request an extension prior to the October deadline. The latter development has not been finalized, but for now it seems like the risk of a hard Brexit, which increased with the election of Boris Johnson, has been tempered. While the British Pound and UK markets rallied on this news, there is likely more volatility in store between now and October 31st. Boris Johnson is not one to go down without a fight.