Can a Bull be Tamed?

The equity bull market continues to run, and in a very tame fashion. Since the bull market began in 2009, U.S. large cap stocks have posted gains in every single calendar year. And with double-digit returns under our belt thus far in 2017, we are well on our way to extending that annual winning streak to 9 consecutive years. The recent stability has been most impressive—September marked the 18 th month of the past 19, in which the S&P500 posted gains, including every single month this year. One could get used to this sort of thing. But should they?

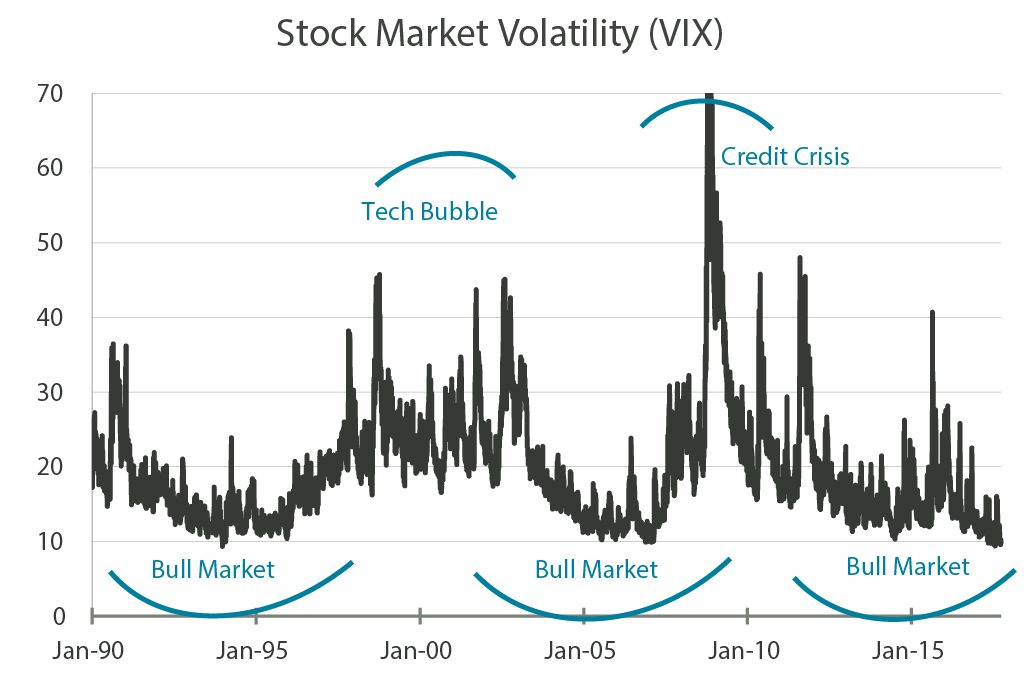

A placid bull market trots along. It has been a while since stocks experienced a meaningful drawdown—the S&P500 has not undergone an official correction (a decline of 10% or more) since early 2016. In and of itself, that timeframe is not particularly notable, as corrections have historically occurred about every 18 months. But prior downturns have not always been evenly spaced out—if you recall, we went nearly four years without a correction between 2011 and 2015. Despite various worries which come and go, extended periods of low volatility are not unusual in bull markets. Therefore, with regards to frequency, there is nothing that suggests we are “due” for a meaningful pullback in stock prices. While perhaps not ever being fully domesticated, a bull can certainly act gentle and tame for long periods of time.

Low volatility can be ironically unsettling. It is not the length of time between corrections, but the fearlessness of markets that has many investors shaking their heads. Especially as the extraordinary lack of volatility over the past year and a half contrasts against a variety of ongoing macro uncertainties (including domestic political issues, fiscal policy delays, a tightening Federal Reserve, North Korea tensions, Brexit, stock valuations, etc.).

The S&P500 has gone more than a year without even a 5% pullback, the longest stretch in more than two decades. Meanwhile, the CBOE Volatility Index, a popular measure of implied volatility (sometimes called the “fear index”), is hovering near record lows. The VIX dropped to an intraday reading of 8.8 towards the end of July—its lowest level in history. It is worth mentioning that volatility is subdued across a variety of asset classes, not just stocks.

Now, a dearth of volatility in the face of a seemingly uncertain world can feel quite strange, but it is not necessarily unusual. Nor is low volatility in and of itself always a sign of investor complacency—it can sometimes simply be the result of a confluence of market-friendly conditions. With regards to the recent environment of low volatility, the massive amounts of central bank liquidity subsequent to the 2008 credit crisis encouraged investor risk-taking (historically low interest rates provide few alternatives to stocks). Yet middling economic growth and a dearth of inflation kept the Federal Reserve from moving too aggressively to tighten monetary policy. It is this combination of massive liquidity and stable—but not overheating—growth that, since 2009, has overwhelmed political and policy uncertainties and suppressed market volatility. Many would argue that the Fed has essentially beaten the bull into submission.

While both of these components are still largely intact (for now), it would be a mistake to think that low volatility will continue forever. Volatility is often exceptionally subdued for long periods when the economy is between recessions and stocks are in a bull market, but it will almost certainly spike during the next crisis or economic contraction. In the meantime, some worry that potentially dangerous complacency, as a result of the extended placid environment, might be settling in. The tame-acting bull, with the Fed acting as a matador, may have some investors fooled that it will never again become unruly.

Could a Stampede Occur? Make no mistake, an equity pullback could occur at any time for any variety of reasons. We are not just throwing rain on the bull market parade—periodic corrections are a normal part of a healthy market environment. Investing is often a “two steps forward and one step back” process, and a breather in prices can allow fundamentals to catch up while keeping investor sentiment in check. Intermittent and unpredictable stock corrections also help reset valuations and shake out weaker investors, supporting a healthier investment environment and allowing bull markets to stretch on.

However, if/when a correction occurs, any investor complacency as a result of low volatility could make things worse. Misidentifying a care-free market going straight up as risk-free, some investors may be instilled with a false sense of security, stretch for extra return, and unwittingly take on additional risks or imprudent amounts of leverage. Undisciplined investors may become vulnerable to unanticipated shocks, and given how few and far between corrections have been during this bull market, even a run-of-the-mill price dip or correction may be extremely nauseating and panic-inducing for some. In this day and age of passive investing, algorithmic-based trading, and media-driven herd behavior, any sell-offs could also be particularly sharp and provide investors little time to react. A sudden frenzied rush out of equities (for whatever reason) by a mass of panic-stricken investors could lead to a sharp spike in volatility.

If the Bull Bucks, Hold on Tight. So do we think a correction is in store? Perhaps, though pinpointing a specific cause may be difficult to ascertain. Solely from a seasonal perspective it would not be surprising to see a return of some volatility as we head into the winter months. Furthermore, the Federal Reserve is about to initiate a reduction to their balance sheet, which may in effect remove some of that liquidity backstop that has limited volatility for so many years. As with any Fed policy shift, an increase in volatility surrounding the change would not be surprising. These, in combination with other macro concerns, could spur a sell-off.

However, should a pullback occur, we believe that once the potential threat (whatever it is) dissipates the bull market should continue as long as economic progress and corporate earnings improvements stay intact. Especially as we are not seeing too many signs of extreme complacency such as undue leverage, weak underwriting, or the mass creation of misunderstood financial products. For now, our base case is that volatility may creep higher but the bull market should keep running (albeit with less stellar returns going forward thanks to elevated valuations).

Successful investing involves an acceptance that one may occasionally lose money in the short run. The key is to do so without panic. In real life, bulls may act tame and gentle for periods of time but are rarely fully domesticated— bulls have bad days too, are born to buck, and take joy in unseating even the most confident cowboys. Don’t let the stock market do the same to you.