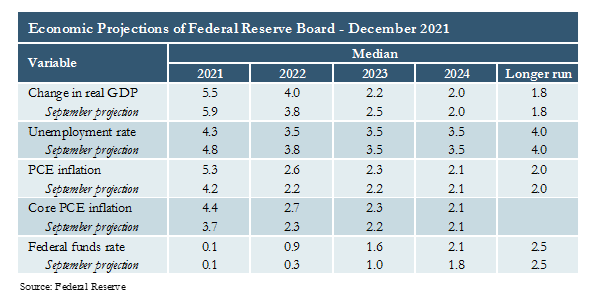

What should we make of these central bank actions? First, the good news. The employment environment has improved a lot since the massive job losses caused by the pandemic. Enough so that central banks, particularly the Fed and BOE, are feeling like they have met that portion of their mandate. Unemployment rates in the U.S. and U.K. are both nearing 4%, a historically low level. The European Union sits closer to 7%, with only Greece and Spain showing unemployment rates above 10% as of September 2021. Besides a mandate to support employment, central banks have a responsibility to maintain stable prices. Since the Global Financial Crisis (‘07-‘08), the biggest challenge was to grow economic activity enough to support an inflation rate of around 2%. Inflation rates have far surpassed those levels in the past year, forcing central banks to re-evaluate how much monetary policy may be contributing to that and how to adjust appropriately.

What this doesn’t highlight however, is that a lot of people have dropped out of the labor force, leaving a record number of job openings (over 11 million in the U.S.). Businesses are currently faced with the need to pay higher wages and the challenges of finding and/or keeping employees in this environment. As coronavirus concerns and policy measures persist, we continue to suffer from the inadequacy of the supply chain to keep up with the pace of the rebound in demand for goods and services. These factors contributed to the heightened pace of inflation which has central banks on their toes, recognizing that inflation may not be as “transitory” as they had hoped.

In our opinion, central bankers would love to drift more into the background where investors don’t hang on their every word. They are hoping that market forces create a more sustainable economic environment from here that doesn’t require so much intervention. The last thing they want to do is spook the markets by doing something unexpected or moving too far too fast. But they would also like to get back to a more normalized rate environment in due time as they recognize that their emergency measures can lead to irrational behaviors. Although each of the central banks discussed above captured different headlines with their announcements this week, they are all leaning in the same direction, just moving at a slightly different pace.

How are we positioning portfolios for the evolving economic environment? We have discussed before that investors need to be mindful of the challenges to core fixed income in a rising rate environment, particularly one with heightened inflation, where both nominal and real (inflation-adjusted) returns will face significant headwinds. Additionally, equity prices may face headwinds as interest rates increase as there is typically an inverse relationship between interest rates and Price-to-Earnings multiples. However, historically speaking, interest rate increases starting from such low levels are usually tied with above average growth rates, which may buoy equities somewhat. Key investment themes for us include maintaining low duration risk in core fixed income combined with exposure to strategies that offer positive real yields in the case of a higher inflation environment, such as private income strategies. In equities, a bias towards active management and/or non market-capitalization weighted indices and undervalued businesses that may still benefit from a further recovery including developed non-U.S. equities, offers a better risk-reward trade-off.

Please see the PDF version of this article for important disclosures.