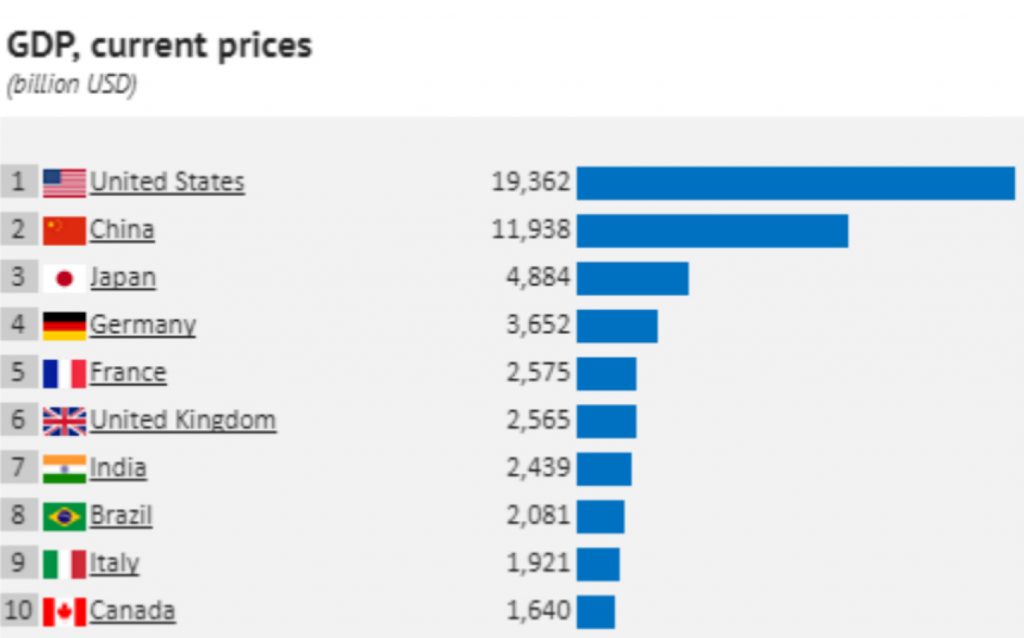

It wasn’t that long ago that China was the world’s largest economy. In fact, it relinquished that crown to the U.S. around 1890. The Chinese economy went into somewhat of a slumber until the end of the Cultural Revolution under Mao Zedong in the 1970’s. Since then the Chinese economy has followed a more market-driven economic path and has prospered, sometimes growing GDP by more than 10%. Its economy is still growing at greater than 6% despite having grown to nearly the size of the U.S. (some argue it has already surpassed the U.S.).

Why, you might ask, is China so underrepresented in portfolios relative to the size of its economy then? At present, China represents approximately 30% of the MSCI Emerging Markets Index (after the MSCI China Index gained more than 50% in 2017). The 12-month forward P/E for China sits at just 14.5X (as ofFeb 1st) relative to the U.S. which trades at 18.8X. Keep in mind though that China is anticipated to grow its GDP by some 6.5% compared to estimates for the U.S. in the 2.5-3.0% range. Isn’t 30% of the MSCI Emerging Markets Index a significant share for China? Yes, and no.

If you look at the MSCI All-Country World Index, China makes up only 4.2% of the total index capitalization. The United States by contrast makes up 50% of the index. Despite being at least the second largest economy by GDP, China is the fourth largest company represented in the MSCI All Country World Index with Japan (8.07%) and the United Kingdom (4.99%) taking up larger portions of the pie.

Source — World Bank, IMF

There are many arguments for why China is not a larger portion of the index including liberalization of financial markets, free movement of capital, rule of law and the fact that China is a single-party state controlled by the Communist party

We can all agree that these are reasons to be cautious about investments in China. The fact that China represents such an underweight in the global indices also suggests that there may be a real opportunity for investors that can get comfortable with the risk factors. The size of the consumer market in China along with the rapid pace of growth and development in the country offer potentially larger opportunities for growth than any of the Developed Market economies. In the Fall of 2017 President Xi Jinping was re-elected for a second term and it is highly anticipated that since he did not appear to nominate a successor at this time that he will likely vie for a third five-year term in 2022.

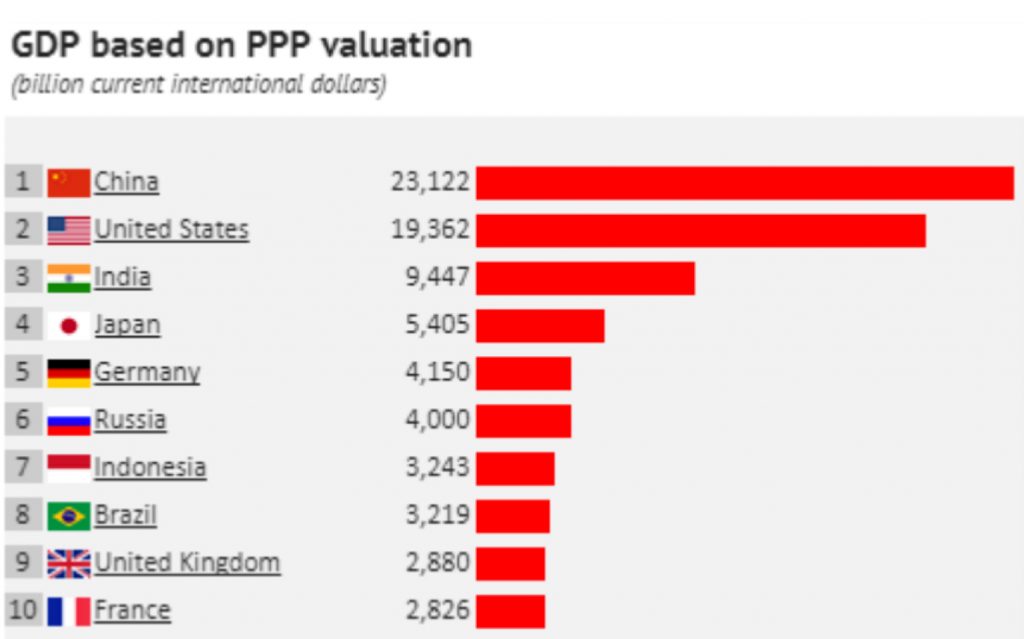

International dollars measure varying purchasing power parity based on a global basket of currencies.

Source — World Bank, IMF

This would require some constitutional changes as there is currently a two-term limit. If the scenario plays out as anticipated, it would likely mean a relatively predictable next ten years in terms of key economic priorities. Some of those priorities are known to be focused on scientific discovery including Artificial Intelligence and Biotechnology, where President Xi expects China to be the world leader. Many investors are not comfortable making meaningful allocations to China but they may be missing a real opportunity over the coming years as Chinese equity capitalization is more likely than not to move in the direction of its share of World GDP.

No investment is without risk. However, we believe this opportunity is one worth studying more closely and considering what the possible payoff for those risks may be.