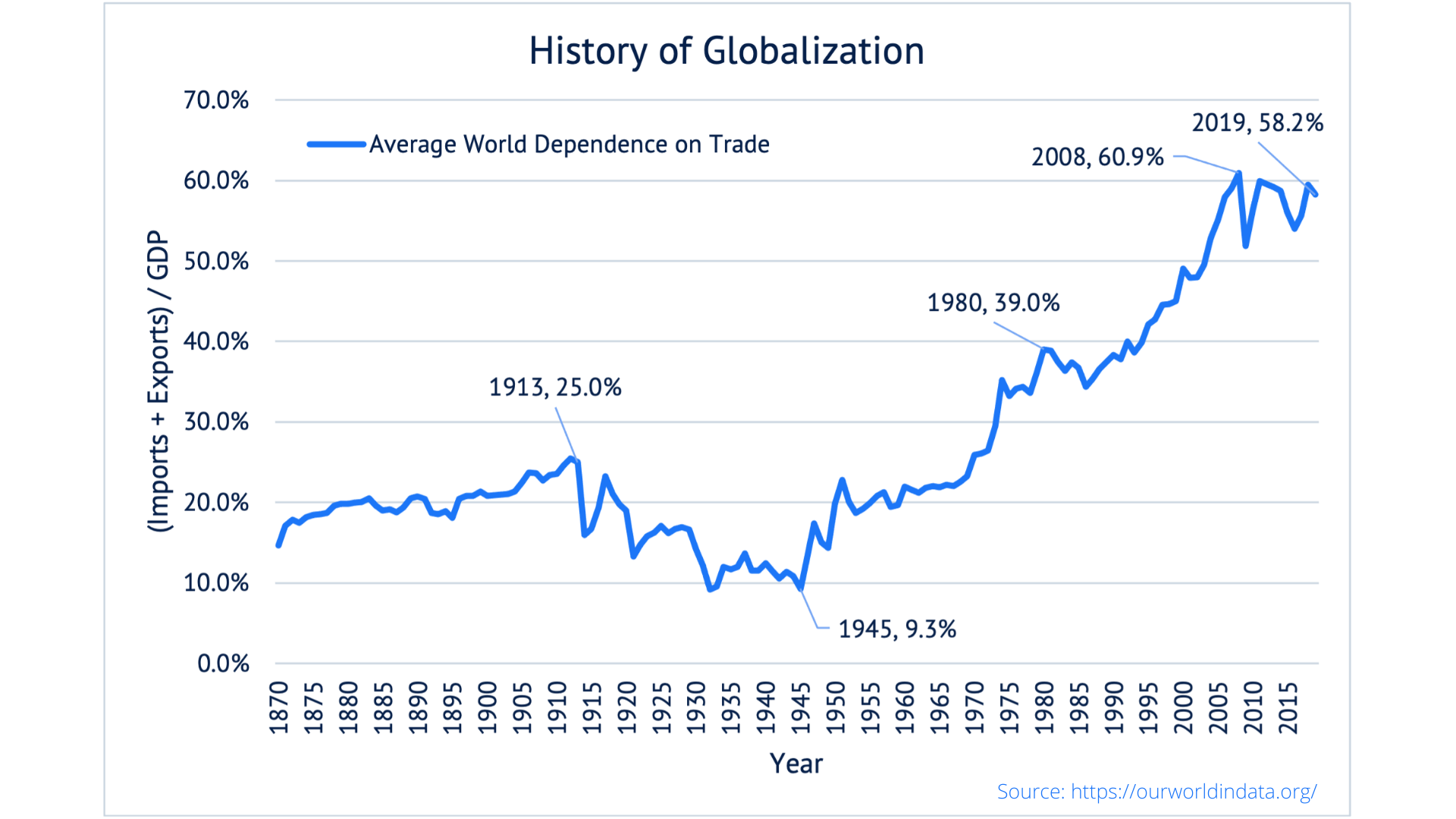

Before addressing the current scenario, it is important to define globalization and put it in context with history. Globalization is the general process of increasing interaction and integration of people, cultures, economies, and governments worldwide. The Globalization super-trend since 1945 has been driven by technological advancements and the reduction in international trade barriers allowing for a global economy where the most efficient participants produce goods and services. Globalization can be measured in many ways, but one of the most common is the ratio of world exports to world GDP. By this measure, globalization increased steadily since the conclusion of World War II up until the global financial crisis in 2008.

Since 2008, a slow deglobalization trend has emerged but only recently caught investor attention. This trend began with an increasing focus during the past decade on the modernization of China’s economy into a service-based economy rather than an outsourced producer of goods under President Xi Jinping. The trade war between the U.S. and China in 2018 further escalated this trend (insert a link to prior paper). More recently, the COVID-19 pandemic exposed weaknesses of reliance on global supply chains. As consumer spending shifted and government lockdowns limited the ability to transport goods, companies that rely on overseas supply chains were caught without critical components. Ever profit-seeking, one would expect corporate behavior to respond and bring more of that supply chain to the local level to insulate from further disruptions. Amid the recovery from the pandemic, the invasion of Ukraine highlighted the risks of global supply chains at the geopolitical level. Europe was caught dependent on natural gas from Russia, making it unable to apply full sanctions without exposing themselves to an energy crisis. The fiscal response was quick. Just three days after the invasion, German Chancellor Olaf Scholz announced a significant shift in the country’s energy policies directed at reduced dependency on single external suppliers and increased defense spending budget. While Germany was the most exposed to this dependency, we believe there will be a renewed focus from political leaders globally on economic independence.

What does this mean for investors?

We believe the risks of a global recession as a direct result of the conflict remain low, but we do have to consider whether this event could have knock-on effects. We keep a close eye on our Market Cycle Dashboards each month for hints that recession risk is increasing. Recessions take time to develop, but we continue to see a low probability of recession over the near term. Putting Russia’s economy into perspective, coming into 2022, it represented less than 3% of the MSCI Emerging Markets Index, representing approximately 0.3% of the world market capitalization. Russian GDP is approximately $1.5 Trillion, similar in size to Canada, Australia, or Brazil. Russia’s top exports are oil and wheat. The U.S. imports less than 4% of Russia’s goods for sale, or approximately $14.5 billion per annum. China is the largest importer from Russia, with the Netherlands, Belarus, Germany, and Italy rounding out the top five. As a result, most investors will be little impacted by the collapse in Russian equities because it will represent a minuscule allocation in any portfolio.

If a recession is not imminent, certainly deglobalization should contribute to a slower growth environment? While many public figures have warned about the potential negative impacts of further deglobalization, we believe there may be near-term drivers of growth from increased government spending and capital expenditures associated with onshoring supply chains. Legislation to boost government spending on renewable energy infrastructure, semiconductors, defense, and healthcare innovation is already on the table and has increased the likelihood of support. In addition, as corporations reorganize their supply chains, capital expenditures are likely to create opportunities for infrastructure development, demand for new jobs, and profits for those companies positioned to benefit. While not the most efficient path for growth over time, we believe these trends provide a stimulative backdrop for the economy.

These growth opportunities will need to be balanced against their natural inflationary pressures. We must deal with the reality that our labor market is already tight. While bringing supply chains back to the U.S. may lower our dependency on foreign suppliers, it increases the risk that we will not have the labor market to support the necessary growth and spending. Some corporate profits could see near-term pressure from the increased cap-ex associated with supply chain reorganizations; other industries and companies may be poised to benefit from that spending. From a cultural perspective, as countries face inward, we risk further isolation and the potential for decreased diplomacy and cooperation at the geopolitical level. While these concerns are legitimate and must be carefully considered, we believe the U.S. is relatively well-positioned to weather a deglobalization trend with a diversified economy and abundant natural resources.

As with any current event, it is important to put recent events in the context of longer-term trends. While deglobalization is catching headlines today, this trend has been building over the past decade, a period of sustained corporate profits, economic growth, and market resilience. The Federal Reserve’s job is more challenging than ever, as its ability to balance inflation, growth, and investor expectations will be critical to navigating the current environment. With so much in motion, we expect volatility may continue and winners and losers to emerge at the company and sector level. In this market environment, we place heightened value on shorter duration fixed income portfolios, with dry powder available to take advantage of opportunities as we navigate these markets for clients. Globally, we believe the economy will find balance over time, and demographic trends paired with continued technological innovation will keep a lid on inflation over longer time horizons.

If you have any questions, please contact us.

Please see the PDF version of this article for important disclosures.