Insurers Exiting Vulnerable Areas

One of the foremost challenges facing the home insurance market today is the departure of carriers from certain regions or segments. This trend has been driven by a confluence of factors, including increasingly frequent and severe natural disasters such as wildfires, hurricanes, and floods. The U.S. experienced 28 disasters costing $1 billion or more in 2023, causing a total $92.9 billion in damages. For perspective, the 1980-2023 period averaged just 8.5 billion-dollar events per year. (Data from National Oceanic and Atmospheric Administration.)

In the wake of significant losses, and in expectation that these higher loss levels may be a “new normal,” some insurers have been forced to reevaluate their risk exposure and make strategic decisions to withdraw from markets where they perceive elevated risk. California and Florida are seeing the most severe impacts: At least seven of the largest property insurers in California are declining or severely limiting the issuance of new policies there, and Florida’s insurance market is in crisis, with 11 or more companies having to liquidate since 2017 and others choosing to leave the market.

Further, numerous insurance carriers refrain from underwriting high-value homes. For instance, Frontline, a regional Florida insurer, declines coverage for properties exceeding $2 million in value. Also, such properties are often situated in coveted locales within catastrophe-prone regions. This convergence of limited carrier options and elevated risk exposure is causing dramatic spikes in premiums, prompting some consumers to contemplate self-insurance as a viable option, should coverage be obtainable at all.

Capacity Constraints

Adding to these challenges is the tightening of capacity within the insurance industry. Capacity refers to the financial resources available to insurers to underwrite policies and pay claims. In recent years, insurers have faced mounting pressure from a variety of sources, including escalating claims costs, low interest rates that have dampened their investment gains, regulatory changes, and reinsurer requirements. As a result, many carriers have taken steps to bolster their financial reserves and reduce their exposure to risk, leading to a more cautious approach to underwriting.

Reinsurance Market Discipline

Reflecting the increasingly risky operating environment, primary insurers are also facing tighter terms and conditions from reinsurers. (Reinsurers provide insurance to insurance companies, helping to reduce their risk.) This pressure, coupled with updates to Moody’s Risk Management Solutions’ catastrophe modeling assumptions, is likely to elevate capital requirements for carriers providing property insurance.

2024 Expectations

Looking ahead to 2024, the reinsurance market is expected to be more stable than in 2023, thanks to structural improvements in program renewals including greater retention of risk by primary carriers and lower coverage maximums. These reinsurance enhancements, along with the stabilization of industry premium-to-loss ratios, should bring greater stability to retail pricing and capital deployment beginning in mid-2024.

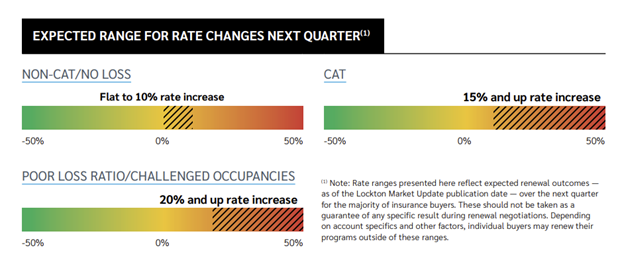

In the interim, according to Lockton Insurance Brokers December Market Update, clients should be prepared for the following range of rate increases:

Source — Lockton

Ways to Mitigate the Impact of Higher Rates

Considering these developments, it’s more important than ever for clients with significant exposure to changing market conditions to work closely with their insurance advisors to navigate the complexities of the market and ensure they have the appropriate coverage in place. This may involve conducting a thorough review of existing policies and exploring alternative coverage options.

Risk mitigation strategies also have an important role to play in safeguarding high-value or catastrophe-prone properties and increasing their market appeal to insurers. This may involve the installation of automatic water shut-off valves, low-temperature alarms, electrical system monitors, clearance of brush from properties situated in wildfire-prone areas, and the implementation of wind protection measures for all home openings in coastal areas.

Moreover, it is imperative to enlist the expertise of an insurance broker when contemplating the acquisition of real estate in a catastrophe-prone region. They can effectively assess the available coverage options, enabling the cost of insurance to be factored into the decision-making process.

In closing, while the home insurance market may face challenges in the months and years ahead, careful planning and consultation with experts can determine the best option for each homeowner’s circumstance to both mitigate risk and manage costs appropriately. Further, this process can and should extend to considerations of tax and estate planning implications, not only cash flow management.

Please speak to your Pathstone advisor to learn more about holistic risk management planning.

Disclosure

This presentation and its content are for informational and educational purposes only and should not be used as the basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to its accuracy, completeness or correctness. No information available through this communication is intended or should be construed as any advice, recommendation or endorsement from us as to any legal, tax, investment or other matters, nor shall be considered a solicitation or offer to buy or sell any security, future, option or other financial instrument or to offer or provide any investment advice or service to any person in any jurisdiction. Nothing contained in this communication constitutes investment advice or offers any opinion with respect to the suitability of any security, and this communication has no regard to the specific investment objectives, financial situation and particular needs of any specific recipient. Past performance is no guarantee of future results. Additional information and disclosure on Pathstone is available via our Form ADV, Part 2A, which is available upon request or at www.adviserinfo.sec.gov.

Any tax advice contained herein, including attachments, is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of (i) avoiding tax penalties that may be imposed on the taxpayer or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.