Key Takeaways:

- The global economic recovery hit some bumps in the third quarter as covid concerns picked up, supply chain issues deepened, China flexed its regulatory muscle and central banks indicated a reduction in bond purchases will start before year-end.

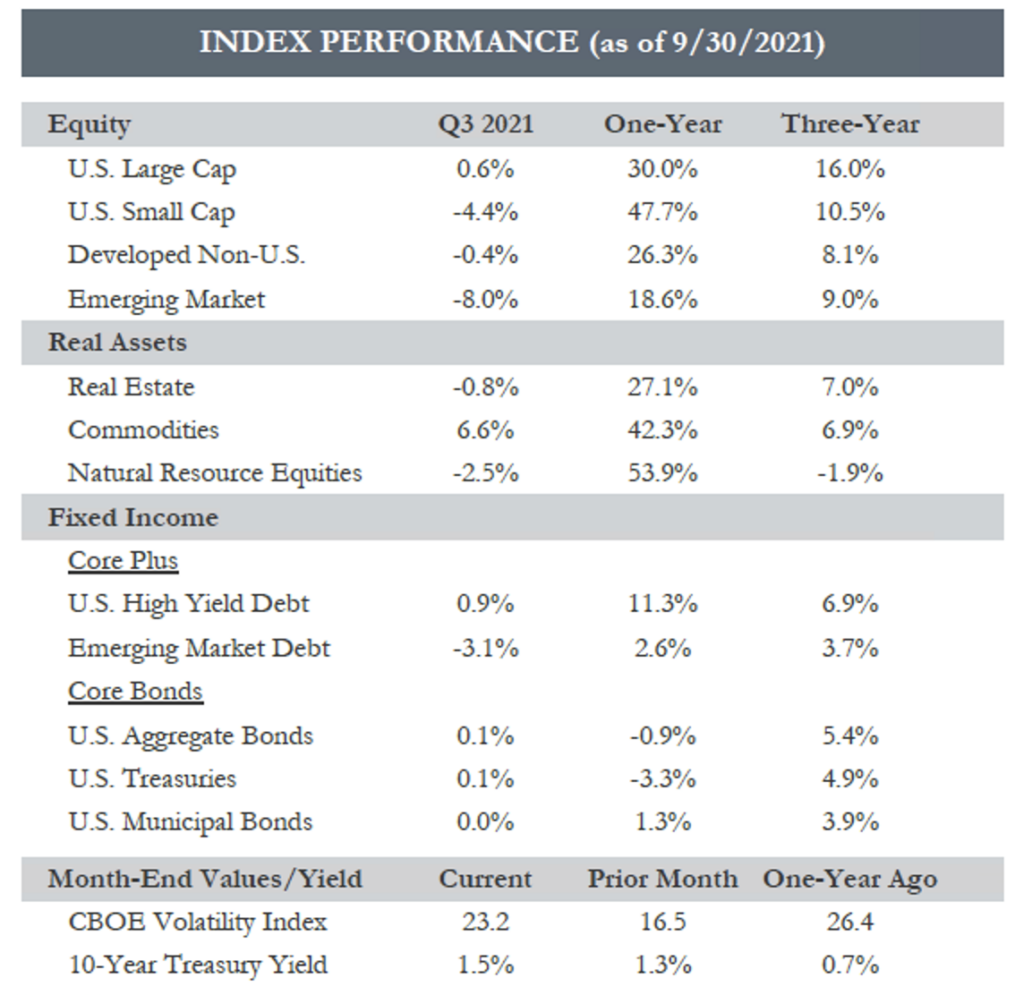

- Global equities lost about 1% during the quarter, with a range of outcomes depending on the market. Japanese equities gained more than 4% while Chinese equity markets fell more than 18%. U.S. Large Caps meanwhile squeaked out a positive return for the quarter.

- Although the year-over-year increase in inflation (CPI) came down a hair in August (5.3%) compared to July (5.4%), that didn’t stop commodities from notching a gain of 6.6% during Q3.

- Despite the heightened inflation rates of the past year, fixed income markets appear relatively sanguine about the prospects for continuing inflation as interest rates retreated most of the quarter, only recovering their starting levels on news of the Fed’s plans to begin tapering bond purchases.

- A pick up in the Volatility Index to end the quarter indicates investor anxieties picking up slightly when it comes to the direction of the economic recovery from here and perhaps concerns about valuations in the face of the recent pick-up in interest rates.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Quarterly Commentary:

- There has been much debate around inflation, particularly as we continue to live in a heavily administered economy, meaning one which has been heavily supported by unprecedented monetary and fiscal policy.

- Interest rates set the tone for decisions around money. When to spend it, when to save it or when to borrow it. The risk is that if the interest rate remains too low for too long it can lead to excessive risk-taking and increases in demand that can drive consumer goods and services prices to higher levels (aka inflation).

- Our central bank, the Federal Reserve is charged with setting monetary policy, effectively managing interest rates, to support economic growth, specifically employment, and maintaining a reasonable rate of inflation. The Fed responded in a significant way to the covid-19 pandemic after many millions of Americans lost their jobs and as the economy was forced into lockdown for a period of time.

- Today we are in a very different place. A large number of people have gone back to work and there are plenty of job openings for those looking for work. Now we are focused on when the Fed will stop its balance sheet expansion (bond purchases) and when it might begin to raise interest rates.

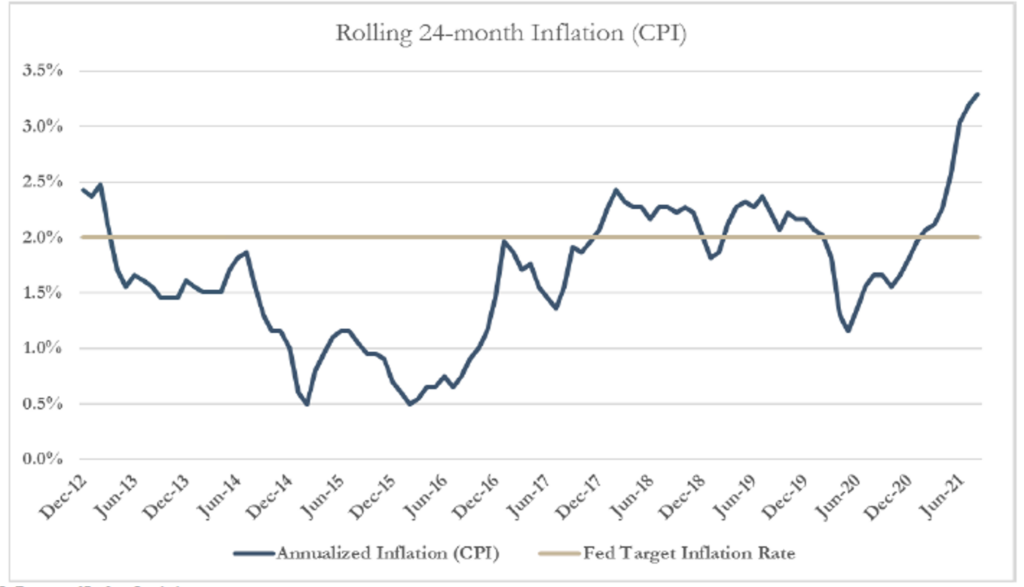

- We have seen year-over-year inflation rates peak in recent months at 5.4% against the Fed’s long-term target rate of 2%. The Fed believes is that the current inflationary impact is more transitory in nature rather than structural. The Fed is willing to allow inflation to run above its 2% target for a while until they are satisfied that the employment picture has improved satisfactorily.

- We believe a look at inflation over a longer time horizon is helpful as well, to see how the Fed is comfortable with the current rates of inflation. The truth is that the 5+% year-over-year inflation readings we are seeing, are skewed in that they are showing the increase from the pandemic lows. That is why we are sharing the below rolling-2-year measure of inflation which highlights that we have spent much of the past decade below the Fed’s target level.

- Our recent report titled: “Taking the Training Wheels Off” highlights that we are near an inflection point in monetary policy and believe market participants will begin to revisit their decision making with a different focus in the months ahead.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved.

Source — U.S. Bureau of Labor Statistics