Key Takeaways

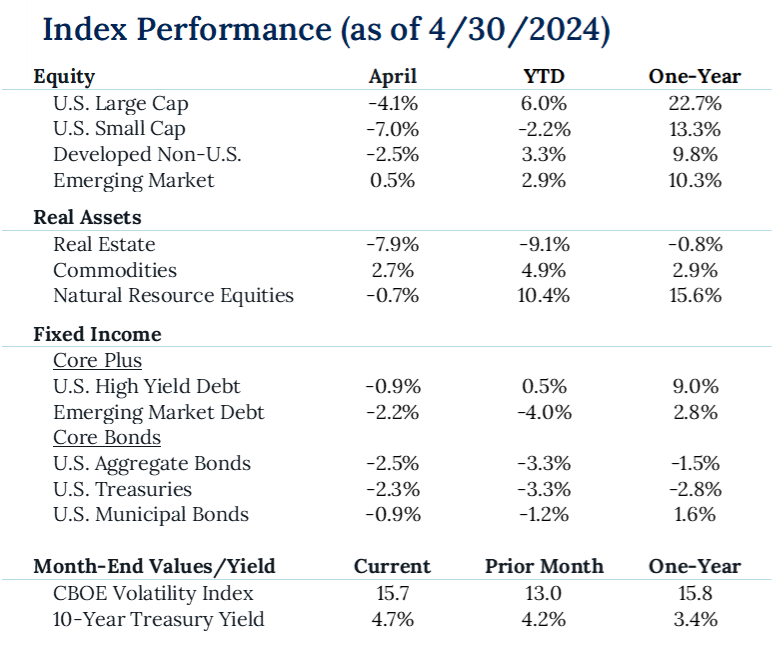

- Market News: April’s mixed economic data threw a wrench in the promising start to the year, causing a significant equity sell-off and raising doubts about a soft landing and the timing of rate cuts. In April, positive data on jobs and the manufacturing sector suggested that the Federal Reserve wouldn’t be cutting interest rates anytime soon. This caused bond yields to rise and stocks to fall. Additionally, tensions in the Middle East and high CPI numbers caused more uncertainty, leading the VIX (Wall Street’s “fear gauge”) to hit levels not seen since October. Despite strong earnings from major tech companies, the S&P 500 failed to end the month in positive territory.

- International Markets: Chinese equities excelled last month as its economy showed signs of improvement. The MSCI China Index is now up +17% over the last 3 months. The recovery of the Chinese economy was reflected in industrial commodity prices such as copper and iron which were up +14% and +17% in April.

- Fixed Income: Bonds continued their suffering as inflation data disappointed and caused interest rates to rise. In April, bond prices fell as 10-year treasury yields rose by 50 basis points. Short-term bonds, which are less interest rate sensitive, outperformed long-term bonds for the month. Junk bonds continued to be the top-performing asset class within fixed income as investors searched for yield.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Disclosures

Past Performance Is No Guarantee of Future Performance. Any opinions expressed are current only as of the time made and are subject to change without notice. This report may include estimates, projections or other forward looking statements, however, due to numerous factors, actual events may differ substantially from those presented. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. Additionally, please be aware that past performance is not a guide to the future performance of any manager or strategy, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. While we believe this information to be reliable, Pathstone bears no responsibility whatsoever for any errors or omissions. Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest. Moreover, the information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. Any investment advice provided by Pathstone is client specific based on each clients’ risk tolerance and investment objectives. This presentation is not meant as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

U.S. Large Cap Equity is represented by the S&P 500 Index, with dividends reinvested. U.S. Small Cap Equity is represented by the Russell 2000 Index. Developed Non-U.S. Equity is represented by the MSCI EAFE Index. Emerging Market Equity is represented by the MSCI EM Index. Real Estate is represented by the S&P Global Property Index. Commodities are represented by the Bloomberg Commodity Index. Natural Resource Equities are represented by the S&P North American Natural Resources Index. U.S. High Yield Debt is represented by the Bloomberg Barclays U.S. Corporate High Yield Index. Emerging Market Debt is represented by the JPM GMI-EM Global Diversified Index. U.S. Aggregate Bonds is represented by the Bloomberg Barclays U.S. Aggregate Bond Index. U.S. Treasuries is represented by the Bloomberg Barclays U.S. Treasury Index. U.S. Municipal Bonds is represented by the Bloomberg Barclays Municipal 1-10yr Index.