- The Federal Reserve raised the Fed Funds rate by 50 basis points in May. This rate hike was mostly priced into the market and did not have a major impact on equity and bond returns for the month.

- The US Economy added 390,000 jobs in May. While lower than the 436,000 added in April, this surpassed estimates of 318,000. In the last week of the month, initial unemployment claims decreased to 200,000 from 211,000 the week prior, while continuing claims fell to 1.31 million, the lowest since 1969.

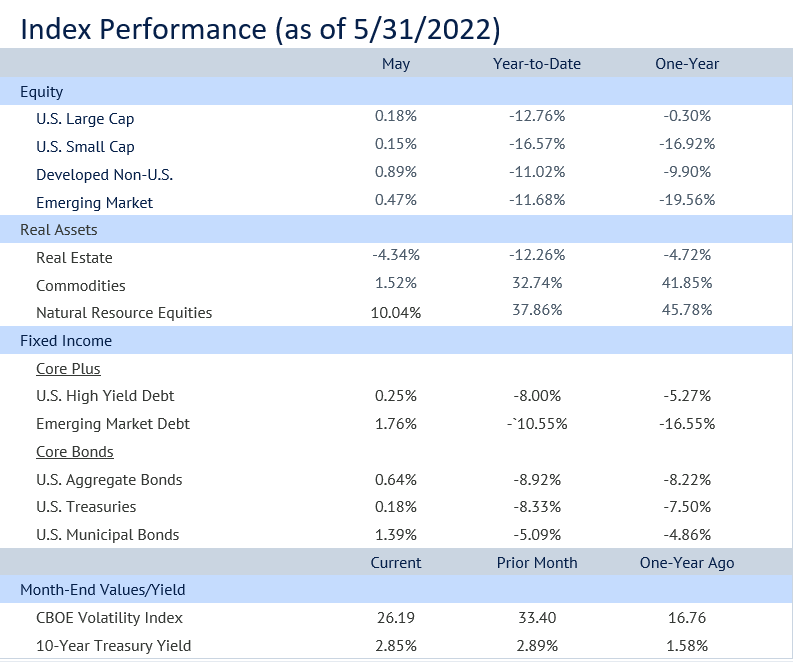

- The S&P 500 started May with a sell-off but in the last week of the month rallied 6% to finish up 0.18%. The Nasdaq had a similar late month rally, but ended the month in negative territory, down almost 3%.

- Volatility is lower than it was last month but remains higher than it was at the start of the year. So far in 2022, about 1 in 6 trading days have closed with a gain or loss of 2% or more for the S&P 500.

- Excluding food and energy, Core Personal Consumption Expenditures increased by 0.3%, rising by about the same rate for three consecutive months. Core PCE increased 4.9% (YoY) in April, which is the lowest level since December 2021.

- Value equities continue to outperform Growth equities this year. The Russell 1000 Growth Index is down 24.8% YTD whereas the Russell 1000 Value Index is down only 4.5% over the same period.

- US Large Cap continues to hold up better than US Small Cap through the past month and year. Along with value, quality of earnings has been an important factor for returns in 2022. Quality balance sheets will be easier to defend against rising rates.

- The Fed confirmed in May that at least two more 50 basis point rate hikes are on the table in the coming months, and they will also release their annual stress test of the banking system later this month. This will give us insight as to how banks are performing in this new environment.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Please see PDF for important disclosures.