Key Takeaways

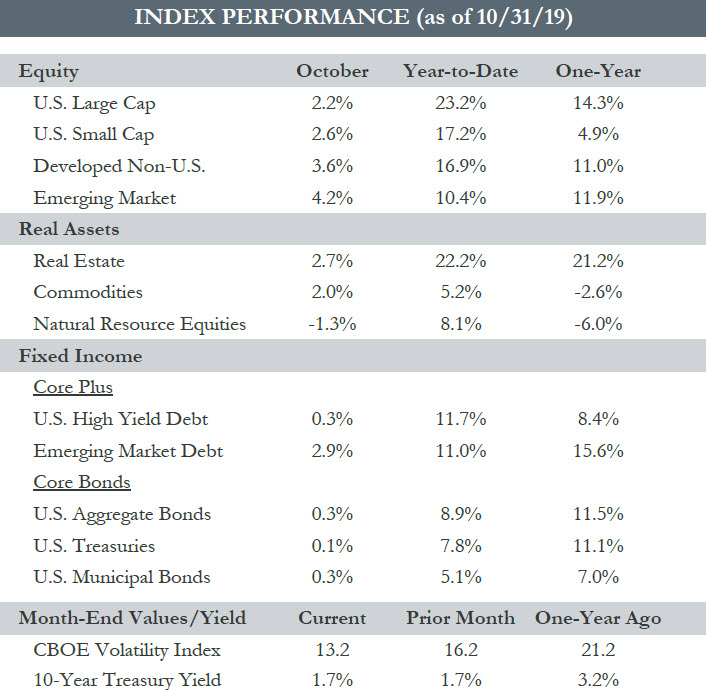

- Risk assets rallied in October as fears of a recession lessened and investor risk appetites improved. Non-U.S. assets outpaced U.S. assets with Emerging Market equities leading the way after lagging for most of the year. The U.S. dollar also weakened versus most major currencies, another reversal in the year to date trend. The S&P 500 made a new all-time high over the month as markets advanced over optimism of favorable news headlines and a potential Phase One trade agreement between the U.S. and China.

- Corporate earnings results for the quarter appear somewhat better than feared. Of S&P 500 companies that have reported earnings so far, roughly 75% have beaten analyst estimates. However, the expectations bar was low and earnings per share are expected to decline by approximately 3% on a year over year basis.

- U.S. Real GDP grew at a 1.9% pace in Q3, beating expectations and keeping with the trend of slow steady growth. Consumer spending continues to be the primary driver of the U.S. economy, offsetting slowing business investment, which has waned with increased global uncertainty. Overseas growth remains sluggish, particularly in Europe.

- The Fed lowered the policy rate for the third time this year, setting the Fed Funds range between 1.5-1.75%. Jerome Powell indicated that Fed officials were comfortable with where current monetary policy stands and no further changes were likely, so long as there is no major deterioration in economic fundamentals or increased inflationary pressures.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Please read important disclosures in the PDF version of this article.