How will climate change affect global financial assets?

Much has been written about the physical impacts of climate change on the planet: heatwaves, droughts, rising sea levels, etc. There has also been growing awareness of the need for action, a need that becomes more urgent every day.

From an investment perspective, the incorporation of environmental, social and governance (ESG) criteria in investment analysis has focused attention on the private sector’s role, both positive and negative, on climate change and related challenges. Financial regulators are also increasingly aware of climate-change risks. Asset managers, notably pension funds, have been in the vanguard of work in this area: for them, the possibility that climate change will reduce the long-term returns on investments makes it a matter of fiduciary duty towards fund beneficiaries.

Unfortunately, change is coming too slowly. The Intergovernmental Panel on Climate Change (IPCC) indicated in late 2018 that warming is occurring faster than projected, and the benchmarks it set (along with the targets set by the Paris Climate Agreement) could be exceeded in as little as 11 years from now. Without massive, structural investment, the world is on course for the point of no return, after which extensive disruption is inevitable, according to the European Geosciences Union.[1] Their late 2018 report cites several scenarios for reaching this point, based on how swiftly the world can switch to renewable energy sources.

Compounding the serious environmental and social risks of climate change are the financial risks. There is abundant and mounting evidence of the financial toll of natural catastrophes. As countries experience increasingly frequent severe storms, flooding and bouts of extreme heat, economic disruptions are becoming increasingly costly. However, unlike the physical impacts of climate change, there is not much in the mainstream discourse about the impact of climate change on global financial assets.

To address this gap, we dug deep into the academic literature. Most of that analysis is highly complex, reflecting a combination of assumptions about the economy, climate change, the physical impacts of climate change, climate-related national policies, and financial assets. We set out to unpack that analysis.

There are two main ways in which the physical aspects of climate change can affect the value of financial assets —impact on (1) physical assets and (2) the production of goods and services:

- First, climate change can either destroy, or accelerate the depreciation of, physical assets (e.g., factories), through its connection with extreme weather events. Physical assets can be directly impacted by floods, droughts and severe storms.

- Second, by interrupting the supply of inputs and labor, it can reduce the production of goods and services, which amounts to a reduction in the return on physical assets.

Further, there is a risk of “feedback loops” between the financial system and the macroeconomy that could exacerbate these impacts and risks, as we discuss in a later section. For example, climate-related damage to assets serving as collateral for loans could create write-offs that prompt banks to restrict their lending in certain regions, which could weaken household spending.

What does this mean for investors? Asset managers cannot simply avoid climate risks by moving out of vulnerable asset classes if climate change has a primarily macroeconomic impact affecting their entire portfolio of assets.

In other words — unless investment dollars are deployed at scale to limit further warming — there’s no place to hide.

What the studies tell us

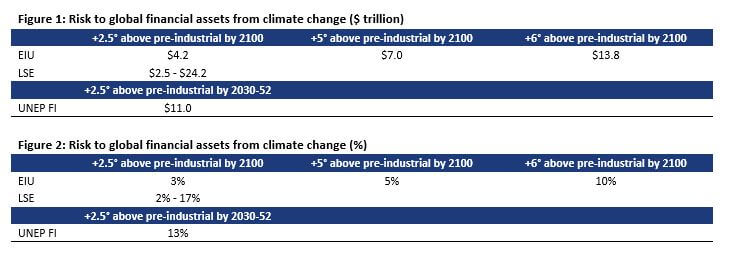

What is the risk to global financial assets from climate change? We evaluated three studies that estimated the risk. In the language of academics this risk is frequently referred to as “climate value at risk (CVaR),” or simply “VaR.” This value is calculated by estimating the present value of financial assets impacted by climate change over a certain period e.g., through 2100. The three studies provide a range of estimates:

- Economist Intelligence Unit (EIU): $4 – $14 trillion at risk from the present to 2100.

- London School of Economics (LSE): $3 – $24 trillion at risk from the present to 2100.

- UNEP Finance Initiative (UNEP FI): $11 trillion at risk from the present to 2030-52.

As a percent of global financial assets, these estimates range from 2% to 17% of assets at risk from climate change. The breadth of this range reflects differing assumptions in the analyses, as shown in Figures 1 and 2. We provide a more detailed review of each study in the sections that follow.

The Economist Intelligence Unit analysis

In order to estimate the relevance of climate change to the asset management industry and beyond, in 2015 the Economist Intelligence Unit (EIU) conducted an analysis[2] of the value at risk from climate change. The EIU estimated the value at risk (VaR) to 2100 as a result of climate change to the total global stock of assets under management. The climate VaR measures the size of the loss a portfolio may experience, within a given time horizon, at a particular probability — e.g., a 1% probability that $24 trillion of global financial assets will be at risk of loss from climate change from the present through 2100.

The EIU used an integrated assessment model built to estimate the economic cost of future climate change. The model links economic growth, greenhouse gas emissions, climate change and the damages from climate change.

To estimate the climate risk at different confidence levels, the EIU researchers acknowledged three key uncertainties, which the academic literature has identified as being particularly determinative of the impacts of climate change:

- The first is the rate of productivity growth, which exerts a strong influence on (1) the size of assets in the future and, through the link between economic activity and carbon emissions, on (2) the amount of warming along a path of uncontrolled emissions.

- The second key uncertainty is climate sensitivity, which is by how much the planet warms in response to a given increase in greenhouse gases in the atmosphere.

- The third uncertainty is the degree of catastrophic climate change that causes severe economic damage.

As per the EIU analysis, the resulting losses to global financial assets in present value terms were $4.2 trillion—roughly on a par with Japan’s entire GDP. That is the average (mean) expected loss, but the value-at-risk calculation includes a wide range of probabilities, and the low probability scenarios are far more serious. Warming of 5°C above pre-industrial levels could result in $7 trillion in losses, while 6°C of warming could lead to a present value loss of $13.8 trillion of manageable financial assets, roughly 10% of the global total.

The London School of Economics analysis

A 2016 study[3] by the London School of Economics (LSE) further refined the EIU analysis in looking at the impact of climate change on asset values.

The analysts used the same integrated assessment model to estimate the impact of 21st century climate change on the present market value of global financial assets. They focused on the same factors that were in the EIU study:

- The rate of productivity growth. Productivity growth influences the stock of assets in the future.

- The climate sensitivity parameter — i.e., the increase in the global mean temperature in response to an increase of atmospheric carbon.

- The link between warming and losses in GDP.

Again, the goal was to obtain an estimate of the climate value at risk, i.e. the risk to global financial assets from climate change.

Their conclusion was, in the business-as-usual emissions scenario — in which the expected increase in the global mean temperature in 2100, relative to pre-industrial, is about +2.5°C — the average risk to global financial assets from climate change is 1.8%. Taking a representative estimate of global financial assets, this amounts to a loss of $2.5 trillion, which is below the EIU’s estimate of $4.2 trillion.

However, the value-at-risk calculation in the LSE study includes a wide range of probabilities. Climate change is a problem of extreme risk: this means that the average losses to be expected are not the only source of concern; to the contrary, the outliers, the particularly extreme scenarios, may matter most of all. In the LSE analysis, at the lowest probability scenario (99th percentile) climate risk is 16.9% of global financial assets, or a $24.2 trillion potential loss.

The UNEP Finance Initiative analysis

A May 2019 report[4] by the UNEP Finance Initiative (UNEP FI) provided “a comprehensive investor guide to scenario-based methods for climate risk assessment.” The report relied on the projection of the IPCC of an increase from the present 1°C above pre-industrial levels to 1.5°C of average warming between 2030 and 2052 (i.e., a total of 2.5°C above pre-industrial levels).

Similar to the EIU and LSE analyses, UNEP FI sought to calculate “Climate Value at Risk” (CVaR) for financial assets under several future scenarios. However, a key difference is that UNEP’s measure “brings together assessment of the physical and policy risks of climate change.”

- On the physical side, the methodology examines the impacts of severe changes in the climate and acute weather events on companies’ operations using business interruption as a proxy.

- On the policy side, it explores policy risk — the cost for companies from meeting countries’ emissions reductions targets.

These physical and policy impacts are then translated into dollar values through financial modeling.

Applying this approach to a “Market Portfolio” that “includes 30,000 equally weighted companies, and hence represents the investable market universe”:

- Investors face as much as 13.16% of risk…The 1.5°C scenario, in line with the latest special report by the Intergovernmental Panel on Climate Change (IPCC), exposes companies to…as much as 13.16% of overall portfolio value. Considering that total assets under management (AUM) for the largest 500 investment managers in the world total USD 81.2 trillion, this would represent a value loss of USD 10.7 trillion.

Note that, while the EIU and LSE studies examined the impact of climate change from the present to 2100, the UNEP analysis was based on the IPCC projection of an increase from the present 1°C above pre-industrial levels to 1.5°C of average warming between 2030 and 2052 (i.e., a total of 2.5°C above pre-industrial levels). UNEP’s estimate of a value loss of $10.7 trillion is in the middle of the range projected by the LSE ($2.5 – $24.2 trillion).

The risk of feedback loops

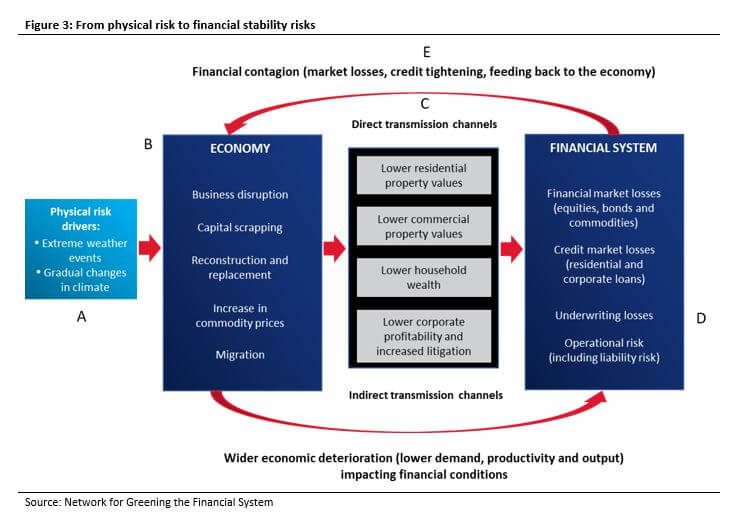

In its first comprehensive report,[5] the Network for Greening the Financial System pointed out that feedback loops between the financial system and the macroeconomy could further exacerbate these impacts and risks. For example, damage to assets serving as collateral (“lower residential and commercial property values,” “C” in Figure 3) could create write-offs (“underwriting losses,” “D” in Figure 3) that prompt banks to restrict their lending in certain regions (“financial contagion,” “E” in Figure 3), reducing the financing available for reconstruction in affected areas. At the same time, these losses could weaken household wealth and, in turn, could reduce consumption.

Implications by sector

As highlighted in a section above, the UNEP FI analysis argued that the challenge companies face from climate change can be broken down into two components:

- Policy risk — the cost for companies from meeting countries’ emissions reductions targets.

- Physical risk — the impacts of chronic changes in the climate on companies’ operations.

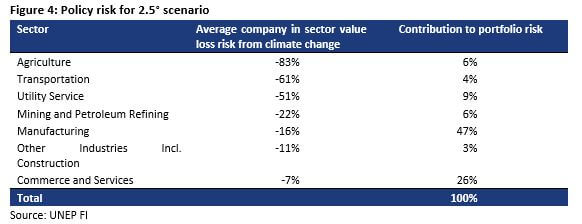

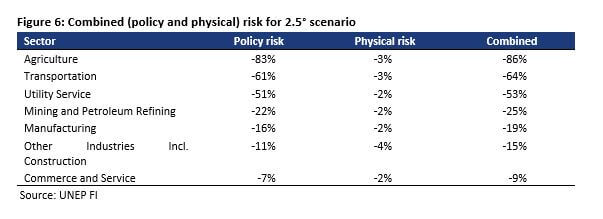

The analysis applied this measure to a “Market Portfolio” of 30,000 equally weighted companies. Figure 4 presents the policy risk for the +2.5° scenario and shows, for each sector, the average company value risk from climate change related policies, as well as the sector contribution to aggregate portfolio risk.

It is at the sector level that climate-related risks become apparent. The Agriculture, Transportation, and Utilities sectors stand out as having high policy risk; i.e., the cost for companies from meeting countries’ emissions reductions targets. Under a 2.5°C scenario, the Agriculture sector is most strongly exposed to policy risk (risk of 83% loss). However, the sector contributes only 6% overall to the portfolio’s climate-related risks, reflecting its low weighting in the portfolio. On the other hand, Manufacturing has a much lower risk of (risk of 16% loss) but has the highest portfolio contribution of 47%.

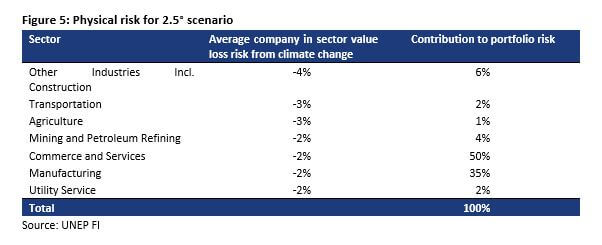

Analogous to the policy risk analysis, sector analysis of the physical risk also shows that the risk differs by sector. Figure 5 shows, for each sector, the average company value at risk from the physical aspects of climate change as well as the sector contribution to aggregate portfolio risk. The results show that the Construction, Transportation and Agriculture sectors have the highest absolute physical loss risk with -4%, -3% and -3% respectively. On the other hand, Commerce and Services, and Manufacturing have lower risk but, based on their weightings in the portfolio, have relatively high portfolio contributions of 50% and 35%, respectively.

Figure 6 combines the two metrics. Not surprisingly, Agriculture and Transportation (air, road, rail, sea), which rank highly in terms of risk in Figures 4 and 5, also rank highly in Figure 6.

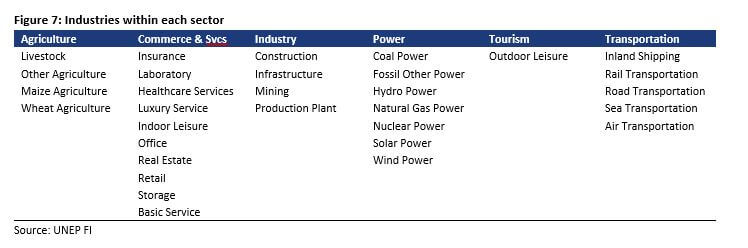

Figure 7 shows the subcategories of each sector, to give a more granular sense of affected industries.

Conclusion

The analyses from EIU, LSE and UNEP FI, together with the work of the IPCC and others to track the pace of climate change, paint a sobering picture. It seems all but inevitable that there will be value destruction in global financial assets in the coming decades. The question remains whether the economic disruptions that will ensue will be mild, moderate or severe. The answer will be determined by the pace at which the world switches to renewable energy and changes other intensive carbon-generating practices.

In the companion report to this piece, Scaling Climate Action: Aligning Investments to Sustainable Development Goal 13, we address how investors can factor climate change into their portfolios. For instance, investing in access to affordable, sustainable and modern energy; safe, affordable and sustainable transportation; and sustainable sources of food and nutrition would positively impact greenhouse gas emissions while mitigating the impact climate change has already had on the world’s population.

Indeed, while we are already seeing the impacts of climate change, we have not yet passed the point of no return from the 2.5°C at which the more extreme scenarios of physical damage and value destruction become a new baseline. There may be no place to hide, but there are plenty of ways to fight.

Please see the PDF version of this article for important disclosures.

[1] https://www.earth-syst-dynam.net/9/1085/2018/

[2] https://eiuperspectives.economist.com/sites/default/files/The%20cost%20of%20inaction_0.pdf

[3] http://eprints.lse.ac.uk/66226/1/Dietz_Climate%20Value%20at%20risk.pdf

[4] https://www.unepfi.org/publications/investment-publications/changing-course-a-comprehensive-investor-guide-to-scenario-based-methods-for-climate-risk-assessment-in-response-to-the-tcfd/

[5] https://www.banque-france.fr/en/financial-stability/international-role/network-greening-financial-system/first-ngfs-progress-report