Stronger documentation, higher base rates, and attractive spreads present continued opportunity for direct lenders to earn attractive returns. On the other hand, signs of stress and dislocation in leveraged credit markets are appearing, which contributing to our belief that 2024-25 may present compelling opportunities in stressed and distressed debt.

Source — Source: Pitchbook.

Below we highlight the drivers of Pathstone’s positioning in Private Credit. For further detail including specific opportunities, please speak with your Pathstone advisor.

Distressed Corporate Credit

Elevated interest rates continue to pressure smaller, unhedged borrowers. Lower-middle market issuers face more acute stress as they struggle to offset floating rate debt costs with EBITDA growth. Corporate bankruptcies are trending to a 13-year high, with downgrade rates from “B” to “CCC” rising to 8% . Rating agencies such as Fitch are projecting default rates of 5.5% across high yield issuers in 2024. Further, consumer credit delinquencies are elevated. Consumer-reliant sectors are already under pressure as the leading contributors to defaults counts in 2023. Risks of a slowing economy exacerbate this stress.

Underlying trends include:

- The underlying credit quality of the High Yield index has deteriorated materially. Approximately 25% of the index is currently rated B- or lower, compared with around 5% of the index in 2008.

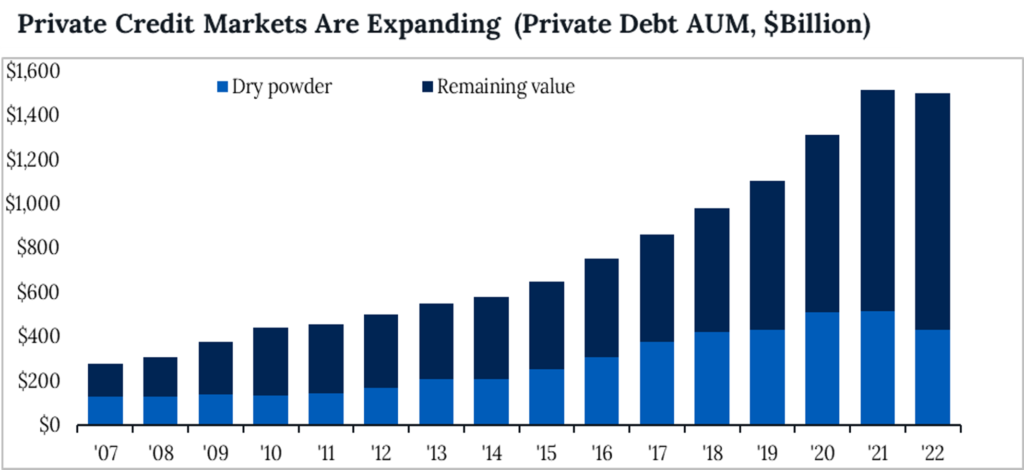

- Record loan issuance over the past several years, often with weak documentation, has also significantly expanded the absolute size of the opportunity set.

Private credit managers are capitalizing on new loan origination opportunities at meaningfully higher base rates. Notably, tighter credit documentation appears to be returning to lending markets.

Vehicle format & liquidity matter. As smaller companies face pressure to service floating rate debt, we remain in dialogue with several distressed, turnaround, and deep value managers poised to capitalize on opportunities to put capital to work.

While the opportunity set appears attractive, it is challenging to time cycles. We continue to prefer well-capitalized and experienced managers unburdened by stressed legacy portfolios. We look for managers we believe can generate strong risk-adjusted returns in benign and stressed market environments, ideally in shorter-duration vehicles (<10 years).

Stressed Real Estate Debt

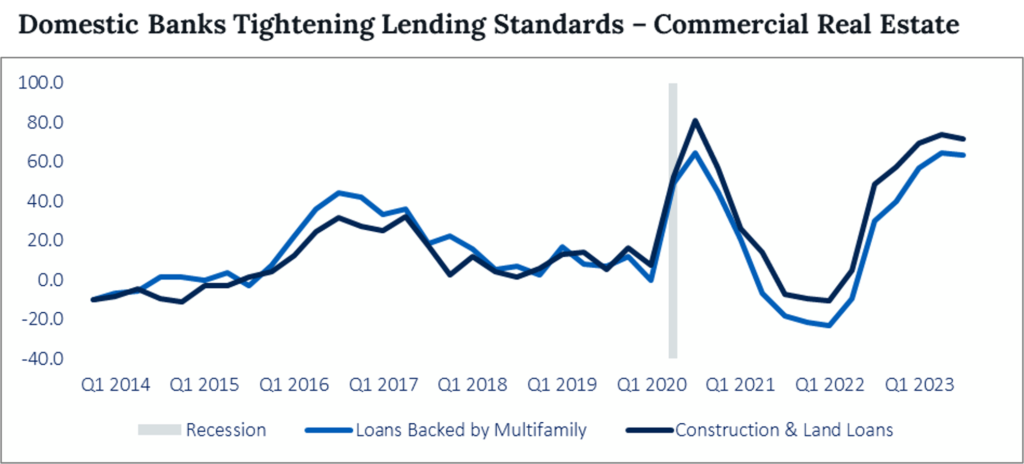

Looming maturities, higher rates and banking stress are driving dislocation in U.S. Commercial Real Estate (CRE) debt markets. Underlying trends include:

- Commercial Mortgage-Backed Securities (CMBS) spreads have widened as borrowing costs and perceived risk remain elevated across several real estate sectors. Non-performing loan sales by banks appear likely.

- Regional banks continue to hold higher concentrations of CRE loans relative to larger peers and remain constrained in their ability to originate new financings.

- Maturity walls arrive while banks are retrenched. CRE loan origination reached peak volumes in 2021-22 with significant regional bank participation. With an estimated $1.5 trillion of US CRE debt maturing before the end of 2025, and interest rate hikes continuing to pressure debt service payments, we expect an uptick in non-performing loan sales.

Source — Source: Federal Reserve Economic Data (St. Louis Fed).

Experienced operators protect on the downside. When acquiring stressed or non-performing loans, we prefer cycle-tested managers able to source off-market opportunities and operate assets if necessary.

Pathstone Allocations

Performing private credit across real estate sectors remains a core allocation in PMA credit portfolios. We are currently allocating to a core all-weather offering with the flexibility to originate private loans or acquire traded securities.

We are also allocating to opportunistic strategies that pursuing distressed corporate credit and stressed real estate debt. Each serves a distinct role in portfolios and can be used together or separately, given prudent sizing.

- In distressed corporate credit, we are focused on a mid-market strategy pursuing restructurings, performing distressed, and spread compression trades.

- For stressed real estate debt, we’re following an opportunistic strategy acquiring U.S. CRE loans from banks along with select traded securities.

Disclosures

This presentation and its content are for informational and educational purposes only and should not be used as the basis for any investment decision. The information contained herein is based on publicly available sources believed to be reliable but is not a representation, expressed or implied, as to its accuracy, completeness or correctness. No information available through this communication is intended or should be construed as any advice, recommendation or endorsement from us as to any legal, tax, investment or other matters, nor shall be considered a solicitation or offer to buy or sell any security, future, option or other financial instrument or to offer or provide any investment advice or service to any person in any jurisdiction. Nothing contained in this communication constitutes investment advice or offers any opinion with respect to the suitability of any security, and this communication has no regard to the specific investment objectives, financial situation and particular needs of any specific recipient. Past performance is no guarantee of future results. Additional information and disclosure on Pathstone is available via our Form ADV, Part 2A, which is available upon request or at www.adviserinfo.sec.gov.

Any tax advice contained herein, including attachments, is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of (i) avoiding tax penalties that may be imposed on the taxpayer or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein.