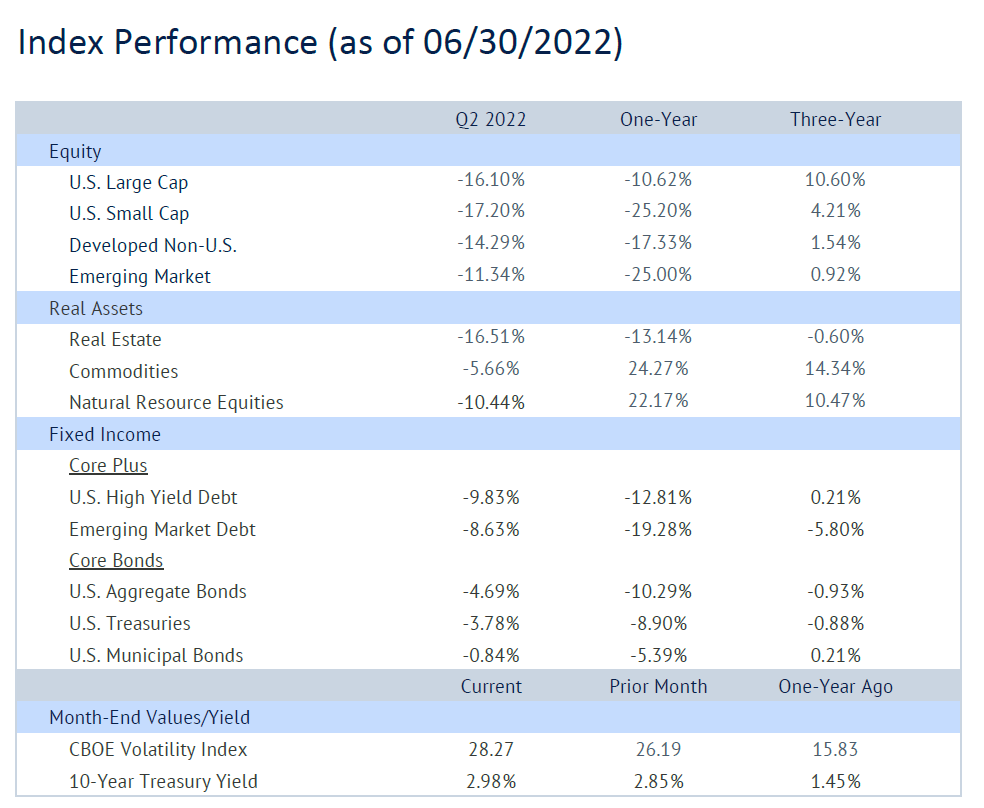

Key Takeaways

- 2022 continues to be a difficult year for investors as both equities and bonds have sold off. Fears of prolonged inflation, increasingly high rates, and the war in Ukraine have left investors feeling anxious.

- Commodities and Natural Resource Equities, which had performed well in Q1 decreased by -5.66% and -10.44% in Q2. Fears of a global recession have brought down prices of cyclical sectors that had solid performance leading into June.

- Core bonds had a negative quarter as interest rates rose. Within stability assets, we continue to have a positive outlook towards short duration fixed income.

- Volatility in markets has picked up again amidst rising inflation, increased interest rate hikes, and fear of a recession.

- The yield on the 10-year treasury rose 0.13% in June and settled at 2.98% after topping out near 3.5% mid-month.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Quarterly Commentary

- The conflict in Ukraine continues to have repercussions around the globe. While commodity prices have fallen since mid-June, they are still at elevated levels. We believe that the U.S. is better positioned compared to European nations to endure the current food, energy, and commodity crunch, but the U.S. is still in a precarious position. Inflation isn’t cooling off the way the market has anticipated, the Fed will push interest rates higher to quash inflation at any cost, and growth is slowing as demand has been destroyed by higher prices. However, we still have an incredibly strong labor market and consumers are currently in a good place financially when compared to the past.

- The most recent headline CPI reading for May came in at a hotter than expected 8.6%. The largest year-over-year (YoY) increases have come from energy prices. Motor fuel is up 49.1%, piped utility gas is up 30.2%, and the prices of vehicles which mostly run on gas are up 16.1% for used cars and trucks and 12.6% for new cars. Food at home prices have increased almost 12%, led higher by meat prices.

- The Fed Funds rate now stands at an upper bound of 1.75% after a 25 basis point (bps) increase in March, 50 bps in May, and a massive 75 bps increase in June. It is highly anticipated that the Fed will raise rates by another 75 bps in July. The last time the Fed raised rates by 50 bps or more three months in a row was during the Volcker years and peak inflation.

- Increases to the Fed Funds rate drove 30-year fixed rate mortgages to over 6%, which is almost 3% higher than the start of 2022. Between high mortgage rates, low supply, and lofty prices, the number of first-time homebuyers has dropped off significantly and the number of investors has picked up. This made the rental market explode and Zillow estimates that rents have increased over 15% YoY. Adjustable-rate mortgages (ARMs) have made a comeback and the percentage of ARMs to all mortgage originations is at its highest level since 2008.

- The 3rd update for Q1 GDP growth came in at a slightly cooler -1.6% (quarter-over-quarter, annualized). The key takeaway was that consumer spending was revised sharply lower, which indicates the economy carried less momentum than previously thought heading into Q2. The Atlanta Fed’s current estimate of GDP growth for Q2 is -2.1% and we will get an official preliminary reading at the end of July.

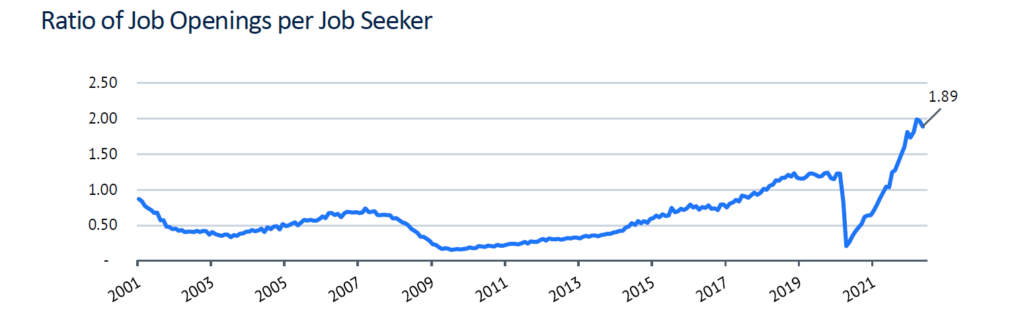

- If there is one saving grace, it is the labor market. We have one of the strongest labor markets we have ever seen with almost two job openings for every unemployed person. Job quits are still near all-time highs, which indicates that people are either realizing it very easy to get a new job or they are very confident they will find one. Layoffs are near record lows because most businesses can’t find enough workers, let alone quality workers to fill job openings. If we do not have a recession or if it is extremely mild, it will be due to the strength of the labor market.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Please see PDF for important disclosures.