Key Takeaways

- News of Omicron prompted an initial shock in early December, but markets quickly rebounded and continued to rally as investors dismissed concerns.

- European officials tightened restrictions in response to the rapid spread of Omicron, while China faces challenges maintaining its “zero Covid” measures amidst the new variant.

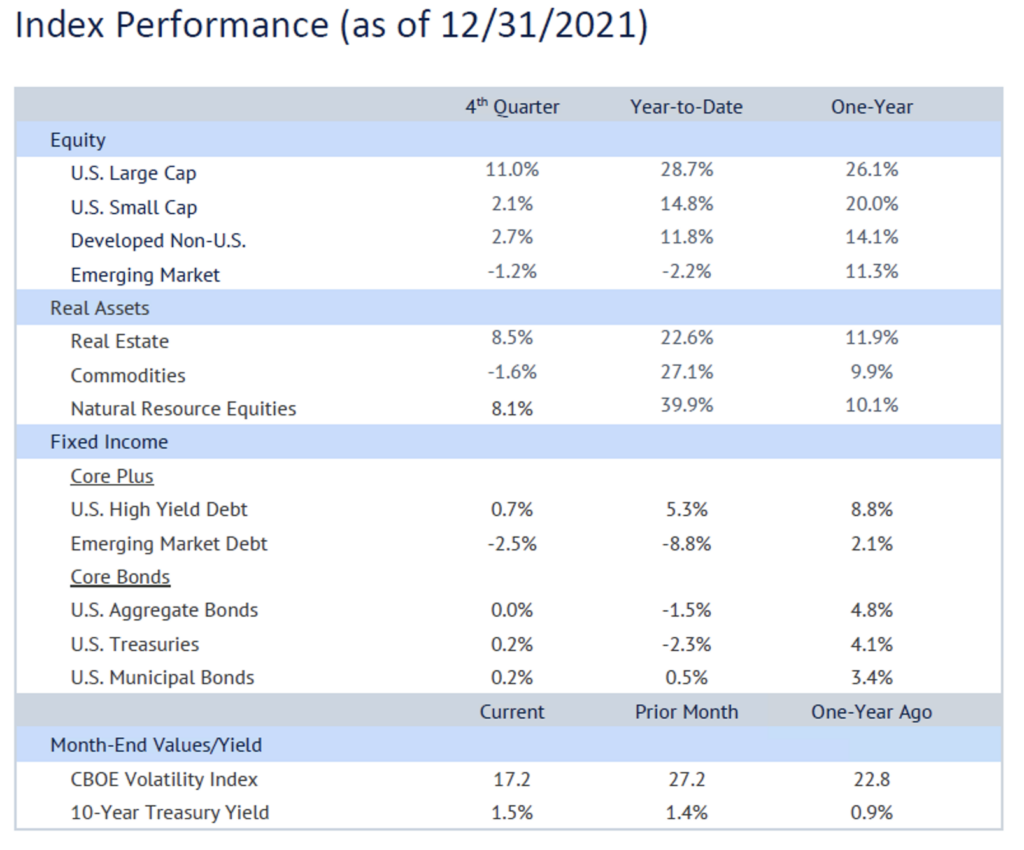

- Despite ongoing health concerns around Covid-19, the S&P 500 gained 28.7% this year and real assets continue to benefit from the reflation trade. Commodities and Natural Resource Equities performed well as economic activity and inflation picked up.

- Core bonds managed a slightly positive quarter as interest rates movements were relatively muted despite central banks indicating plans to curb bond purchases and alerted markets to the possibility of raising rates sooner rather than later. Municipal bonds posted modest gains in 2021 while most other core bond indices ended the year underwater.

- The CBOE Volatility Index, a measure of investor fear, fell dramatically in December after spiking at the initial news of Omicron.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Quarterly Commentary

- The labor market remains challenging for employers with over 11 million job openings and continued wage pressures. Americans are quitting their jobs in record numbers (over 4.2 million quit in November).

- The Infrastructure Investment and Jobs Act was put into place on November 15th, providing a further boost to the labor market.

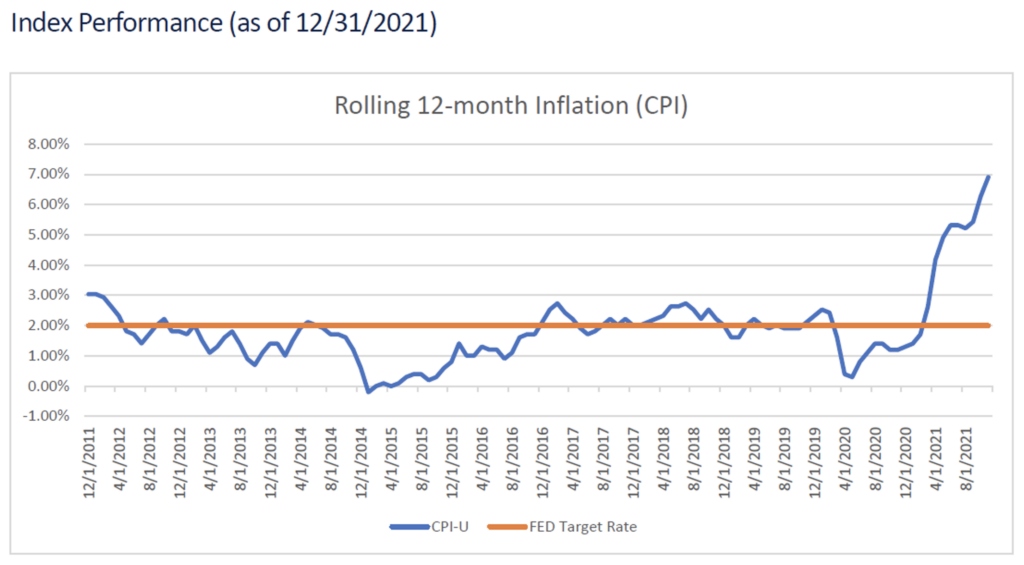

- Inflation rose at a 6.8% annualized rate in November, the fastest pace since 1982. Increased consumer demand for goods combined with ongoing supply chain issues and heightened transportation costs have caused the Fed to reconsider its “transitory” expectations.

- During December’s FOMC meeting, Chairman Powell announced a quicker pace of tapering the Fed’s bond purchases, which will now end by March 2022. Markets are expecting as many as three 25 basis point rate hikes in 2022.

- Despite the Omicron variant, recovery trends are continuing as the global economy is in much better shape than it was last year.

- The focus in 2022 will be on inflation and interest rates as investors dwell on the potential for another year of negative real returns in fixed income.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Please see the PDF version of this document for important disclosures.