Rest assured, this scenario is not a surprise, but rather one that we have spent considerable time thinking about at Pathstone. In this Special Insights note we review how we evaluated our “Fighting (Cyber or Physical) Rattles Markets” scenario and its impact on our outlook. We also provide our assessment of the concerns highlighted above and their potential implications in more detail.

We are actively monitoring price movements to see if they reach attractive levels that would cause us to draw from our liquidity in portfolios to rebalance. Should this situation arise, your advisory team will be in contact with recommendations on how to proceed with a plan specific to your portfolio.

Stress Test Scenario Analysis – Preparing for the Unexpected

“Fighting (Cyber or Physical) Rattles Markets” is a scenario that we considered when we recently updated our Stress Test Scenario Analysis Tool. The scenario description was written as follows:

Geopolitical risks seemed to have largely been put on hold during the pandemic, but we see issues springing up again that are capturing the world’s attention. Cybersecurity risk will continue to grow as more and more of our lives are detailed and controlled electronically. We have seen glimpses of the capabilities that foreign organizations have and must be mindful that these risks will continue to grow. A disruption to a major sector (Energy, Financial, etc) could be crippling and certainly would send ripples through the markets. Expect in this scenario that one will not be able to anticipate which sectors may be more or less directly impacted but presume that fear will lead to a general sell-off of risk assets across the board. Commodities/Hard assets may be one area that not only hold up but could rally in this type of environment. Government bonds most likely would serve as a safe haven in this environment as well, though the magnitude of protection they offer is diminished given the low starting interest rates.

In this scenario, we anticipate that global corporate earnings should be little impacted, but that heightened uncertainty may cause a more meaningful contraction in Price-to-Earnings (P/E) ratios. Inflation may remain elevated in the year ahead (5.0%), and we estimated that the S&P 500 could fall to around 3,810, a roughly 14% decline from the 4,500 level we were hovering near at the end of January. This would leave us with a P/E multiple of 17.7x, only modestly above the long-term average of 16.5x.

Market Reaction

As one would anticipate, volatility has picked up meaningfully in the markets and the initial reaction was a sell-off in equities. Russian equity markets are leading things lower with declines near 25% today. Developed markets are fluctuating wildly with some down as much as 4.5% in Europe, while the U.S. has been rallying off its 2% plus declines at the start of the day to finish strongly in positive territory. Gold, Oil, U.S. dollar and U.S. Treasuries were all catching a bid as safe havens to start the day but eased as investors gauged the situation. Palladium and Wheat, two other commodities where large supplies come from Russia, were getting a price boost as well. The VIX, a measure of volatility, has jumped nearly 10% and currently sits around 32. As of this afternoon, the S&P sits just 10% away from our target price in our “Fighting Rattles the Markets” scenario described above. The markets may take time to further digest this news, so we would caution against making any portfolio moves right away. As the world responds to this news, we are thinking ahead to the next possible set of outcomes.

Can Russia’s Invasion of Ukraine Trip the U.S. into Recession?

As investors, we know that volatility is a part of life, and we are reminded by Sir John Templeton that “The world doesn’t end that often.” What is the potential for the Russian invasion of Ukraine to lead the U.S. or the broader global economy into recession? A U.S. or global recession is not very likely to result from the invasion, but we do have to consider whether this event could have further knock-on effects. Why are we focused on recession? Recessions are environments where real economic damage can occur that takes lengthy periods to recover from and are typically associated with the most significant bear markets (drawdowns of 20% or more). Market volatility or corrections are events we should be prepared for with diversified portfolios and regular portfolio rebalancing. We keep a close eye on our Market Cycle Dashboards each month for hints that recession risk is increasing. Recessions generally take time to develop, but as of now, we see no reason to move into a more defensive mode.

Putting Russia’s Economy into Perspective

Russia represents less than 3% of the MSCI Emerging Markets Index, which means it represents approximately 0.3% of the World market capitalization. Russian GDP is approximately $1.5 trillion, similar in size to Canada, Australia or Brazil. Russia’s top exports are oil and wheat. The U.S. imports less than 4% of Russia’s goods for sale, or approximately $14.5 billion worth per annum. China is the largest importer from Russia, with Netherlands, Belarus, Germany and Italy rounding out the top five. Most investors are going to be little impacted by the 45% year-to-date declines in Russian equities, because it is likely to represent a miniscule allocation in any portfolio.

Impact on Inflation and the Fed

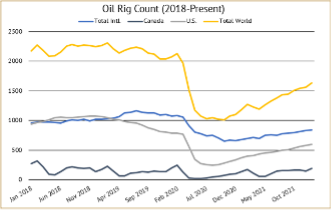

We have seen oil prices spike in response to the incursion into Ukraine. Why? There is a risk that Russia could cut off the pipelines that supply parts of Europe with oil and gas, putting more pressure on the rest of the world’s producers to make up for the gap. Alternatively, Europe may decide to import less as a punishment for Russia’s actions. Oil has historically been a good hedge for geo-political events as it is still the main source of energy, and energy is necessary to keep economies running. The U.S., which made a great push for energy independence, has been increasing the number of oil rigs in service to increase supplies. Likewise, OPEC has been actively increasing its supply quotas. Oil prices were already under pressure as the Baker Hughes Rig Count charts shows that we have not fully recovered the number of operating oil rigs that were in use prior to the pandemic.

The scenarios we explored for 2022 all expected inflation of between 4-6%, a bit higher than the slowdown in inflation the Fed is anticipating. Nonetheless, the recent inflation pressure has forced the Fed to consider raising interest rates sooner and more significantly. Today’s news, however, has changed market participants’ expectations, thinking that the Fed is less likely to make a 50 basis point move in March but still certain that they will make a 25 basis point increase at least. We expect that inflation may be higher for longer than the Fed had hoped; given the ongoing global disruptions to supply chains and the anxiety created by the Russia/Ukraine situation, consumers may be more likely to want to stock up on supplies. We believe that the path of the Fed this year is made a little more uncertain with the disruption in Europe.

World Response and the Evolution of Economies

It appears that the world’s powers are not likely to intervene in the Ukraine militarily, but rather solely rely on economic sanctions as a leverage point to contain Russia’s ambitions. Many nations around the world have condemned the action, though China has been conspicuously silent. While this response leaves some questions unanswered, many question whether this is the tip of the iceberg in terms of a new dynamic including a further push toward deglobalization. Having started during the pandemic, when supply chains which largely ran through China broke down, many countries around the world are reassessing their dependence on other nations and focusing on protecting their borders. This may be a step in the wrong direction in terms of global economic progress and efficiency but could also spur more economic activity in domestic markets. In the near term, from a U.S. perspective this would likely contribute to inflationary pressures as the cost of labor is greater domestically. That said, the current technology revolution may be further accelerated as a necessity to keep inflation under control. We believe the U.S. is one of the best positioned to be able to manage a deglobalization shift with still the most innovative economy from a technology perspective.

Conclusion

This situation opens up a lot of questions forcing us to consider many outcomes both big and small. Investors should take care to focus on the few key decisions that can be most impactful rather than getting tangled up in the minutiae. Diversified portfolios will not be immune from losses but will have some assets that increase in value while others decrease. These types of events are accompanied by heightened volatility given the uncertainty but also often create opportunity particularly for long-term oriented investors. We don’t see this situation as reason to reduce risk as we might if we anticipated a recession. We are actively monitoring price movements to see if they reach attractive levels that would cause us to draw from our liquidity in portfolios to rebalance. Should this situation arise, your advisory team will be in contact with recommendations on how to proceed with a plan specific to your portfolio. If you have any questions, please contact us.

Please see the PDF version of this article for important disclosures.