Both the S&P 500 Index and the Bloomberg Barclays US Aggregate Bond Index (Agg) finished the first quarter of 2018 with negative total returns, in part due to rising interest rates, inflation scares, and tariff talks.

While volatility can create an uncomfortable environment, what’s worse is when investors feel like they have nowhere to “hide” and both stocks and bonds decline in value. Looking back over the past 30 years, it is actually a rare occurrence for both the S&P 500 and Agg to have negative returns in the same quarter. In fact, Q1 2018 was the first time since the third quarter of 2008 where both indices had negative total returns in the same quarter. In the past 30 years this has only happened eight times!

It is unusual for both indices to experience negative returns in the same quarter, in part because stocks and bonds have experienced low to negative correlation, at least this has been the case recently. Despite the conventional wisdom that equities and bonds are negatively correlated, the historical relationship has been much more fluid.

Correlation is a statistical measure used to describe the relationship between two variables. Pairing negatively correlated assets provides a diversification benefit to investors. Negative correlation means when one investment decreases in price, another increases.

In response to the markets’ recent behavior we took a deeper dive into the data to review how these two asset classes have behaved in relation to one another historically by comparing the monthly returns of the S&P 500 to the Agg. Our concern was that the diversification benefits of stocks and bonds might have diminished, leading us to question whether bonds will be a reliable hedge for equities over the next few years as the Fed continues down the path to normalize monetary policy. Historically as investors have become fearful and sold equities they have flocked to bonds as a safe haven. With a muted return outlook and continued rising rates on the horizon this may not be the case over the next few years.

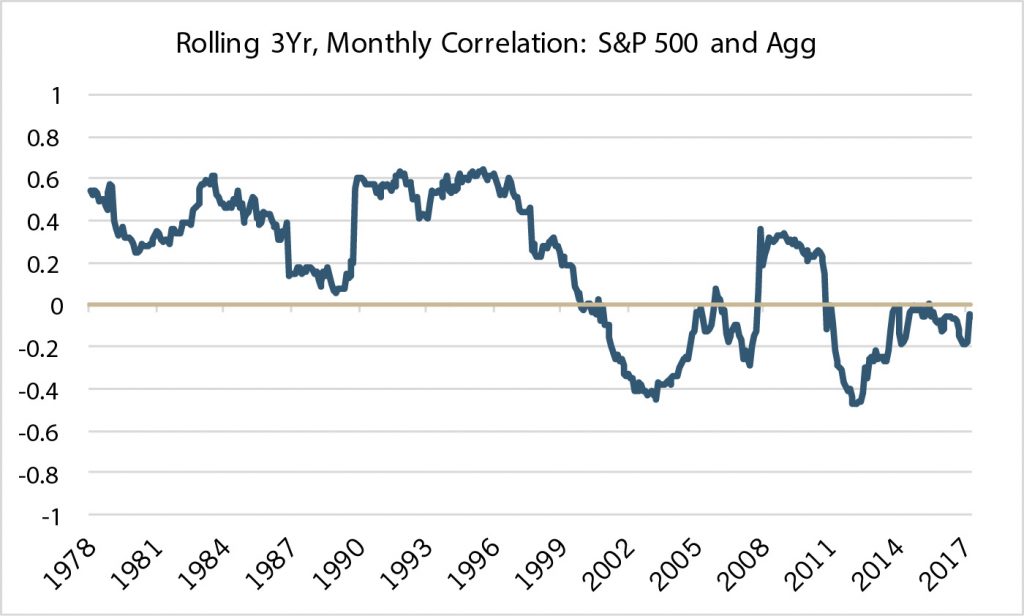

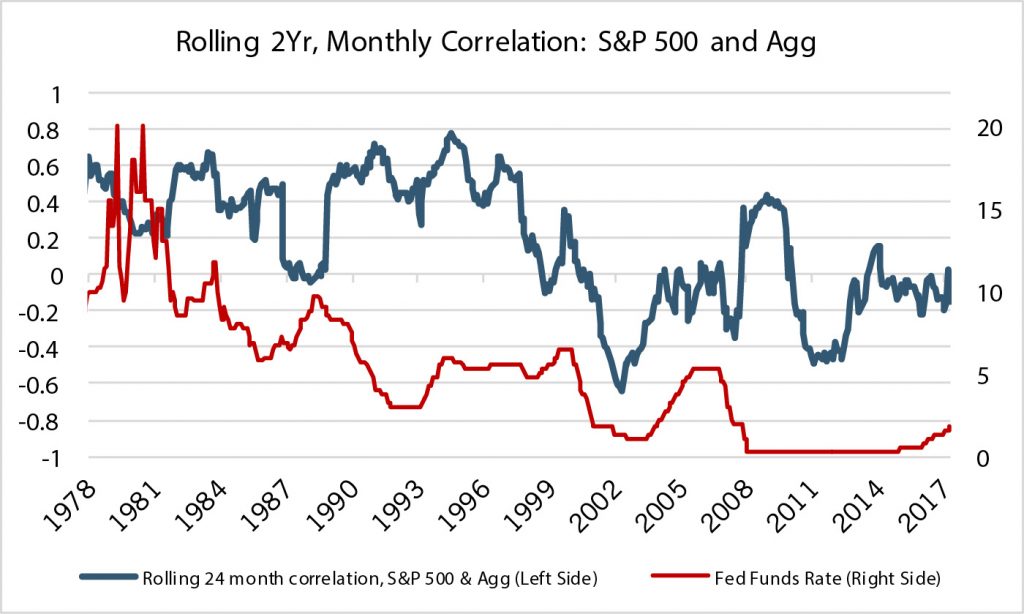

On a rolling three year review of monthly correlations since the late 1970’s you can see that the relationship has fluctuated over time between positive and negative (chart below).

Source — Bloomberg

Throughout the 90’s correlations were heightened as rates fell and stocks were in a bull market. More recently we have seen correlations turn negative around the tech bubble and the global financial crisis, which might not come as a surprise as the Fed drastically cut rates to spur growth in the face of recession

Looking at daily returns for the most recent period shows that correlations between stocks and bonds over the first quarter of this year were negative, despite both the S&P 500 and Agg having negative returns. This means investors have been receiving a diversification benefit.

The chart above shows that since 2015, rolling three year correlations have increased and approached the zero correlation mark.

Quite possibly this is a result of changing monetary policy as the Fed began normalizing interest rates in December of 2015. In fact, in three of the past four periods that the Fed has raised rates, correlations have also increased. With current guidance for several additional rate hikes over the next few years, coupled with the heightened valuations of both stocks and bonds, it would be reasonable to assume that correlations might continue to increase over the near term.

Due to the inverse relationship between interest rates and bond prices, an increase in interest rates causes bond prices to decrease. One explanation why correlations increase in a rising rate environment is that when rates rise the discount rates used to value equities also increase. Higher discount rates decrease the present value of future cash flows, which in isolation, causes equity prices to fall. Since U.S. equity indices have lofty valuations an increase in discount rates could cause a sharp correction, causing both equities and bonds to decline in price at the same time.

Source — Bloomberg

Positive correlations can be a good thing as a rising tide lifts all boats. What investors ideally want are positive correlations in times of rising markets and low correlations when equity markets decline. During equity market declines we would expect fixed income to provide a ballast to portfolios.

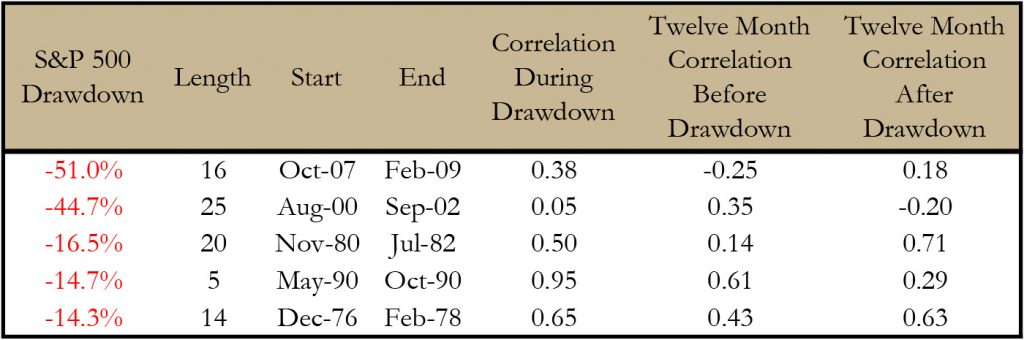

Isolating the five largest sustained drawdowns of the S&P 500 since 1976 show that correlations have risen during extreme market sell offs, with the exception of the tech bubble popping in 2000. This suggests that diversification benefits might break down during extreme market events. Correlations became very high (≥0.5) in three of the five periods.

Source — Bloomberg

Many investors feel like we are “overdue” for the next major correction despite the persistent bull market. While we don’t foresee a recession in the near term, if the correlation trend accelerates and moves into significant positive territory as equity markets suffer a sustained drawdown, investors would not experience the expected diversification benefit.

Luckily though, correlations are starting from a low point. In the lead up to four of the five largest drawdowns, correlations were significantly higher than current levels. The trailing twelve month correlation as of the end of March was -0.21. Despite any moderate increase from here, correlations would still be relatively low. Low correlations would provide a diversification benefit.

In response to the current low return environment we have been shifting exposures within the stability allocation in favor of short duration bonds (cash) and credit risk alternatives as a way to add additional diversification to portfolios outside of traditional fixed income. Short duration bonds, as the name implies, carry less duration than a traditional core fixed income allocation, meaning there is less interest rate sensitivity and as these bonds mature, the principal is able to be reinvested into instruments with increasing rates more quickly. Credit risk alternatives provide exposure outside of traditional municipal and investment grade bonds in strategies such as high yield debt, bank loans, market neutral, relative value, and preferred securities to diversify traditional fixed income risks and maintain liquidity.

We are confident that current stability allocations should provide a hedge to offset equity risk, even with modestly increased correlations. The ever changing relationship between stocks and bonds provides a nice reminder that markets are fluid and the relative behavior of assets can change over time. In a low rate, low return environment we continue to monitor changes in asset class correlations for any potential impact to our tactical decision making.