The Macro Picture

Risk markets have performed very well thus far in 2023 for a variety of reasons. Earnings have held up better than expected, low unemployment has buoyed consumer spending, the Fed has slowed the pace of rate hikes thanks to a steady reduction in inflation, and investors are beginning to unwind bearish positioning. Add to that list the hope that a significant productivity boom driven by advancements in artificial intelligence (AI) technology is forthcoming, and you have a remarkably different market sentiment, including discussions of a new bull market, than witnessed in March during the failure of Silicon Valley Bank (SVB).

Against a 12-month increase of 350 basis points in the Fed Funds rate, the S&P 500 Index has delivered a 19.4% total return – not exactly playbook. It is well documented that a large portion of the gain has come from a small number of technology companies. The more recent broadening of return source suggests either an improvement in institutional investor sentiment or market expectations that inflation will decline significantly in the short-run, supporting strong earnings growth in 2024. Or perhaps both. These short-term positive economic and technical changes since our last communication make our macroeconomic outlook slightly more balanced and reduce, though certainly don’t eliminate, the odds of recession.

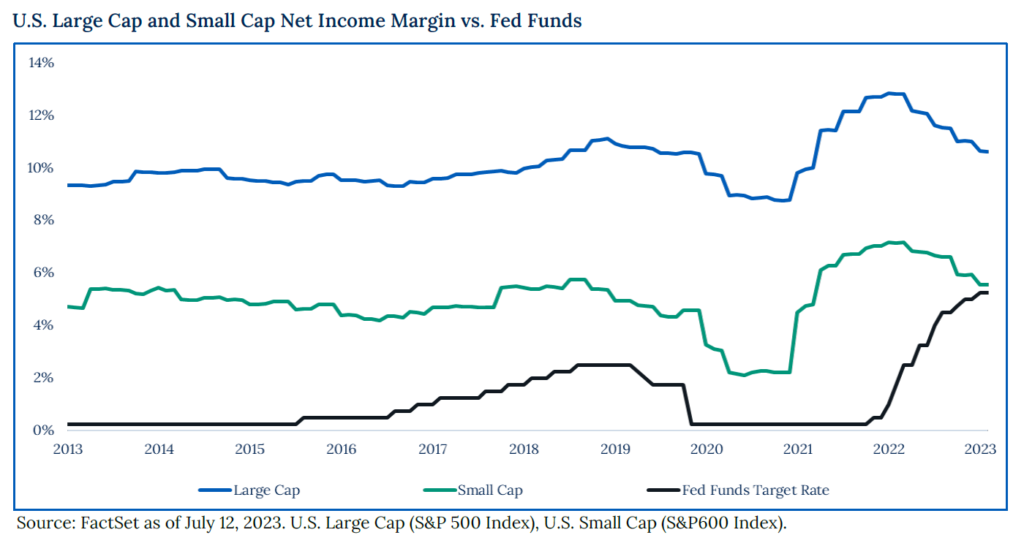

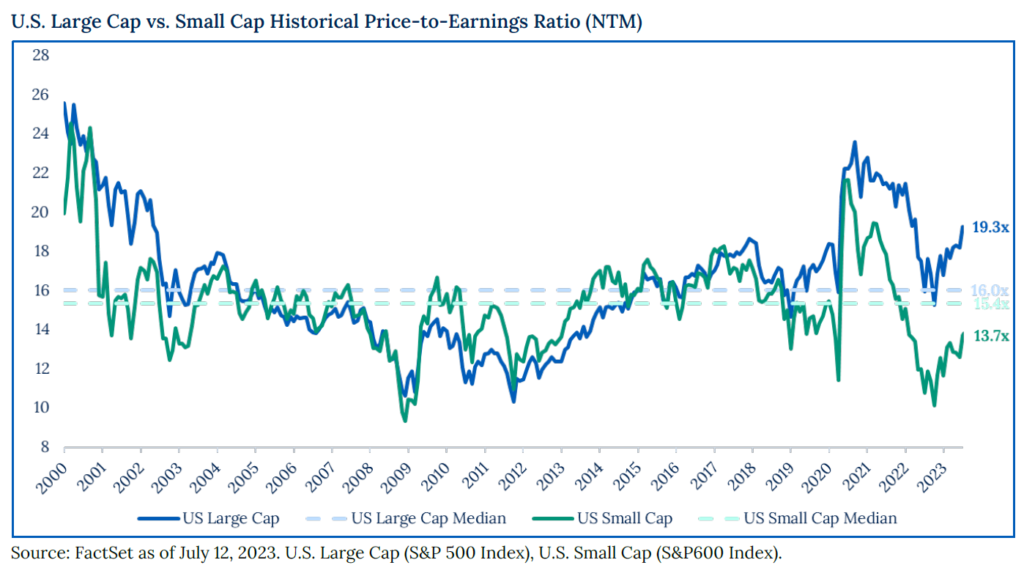

Medium to long-term valuations of Growth assets are determined by interest rates and earnings. The current market multiple is meaningfully higher than the long-term average (roughly 19x vs 16x) and is more in line with a much lower interest rate regime. Coincident with this high multiple is the expectation of a third straight quarter of earnings declines. To justify this backdrop of high valuation and declining earnings, the future needs to be different in (either or both) rates and earnings. We think the Fed’s 2% inflation target is still far away, with uncomfortably high wage growth pressuring rates to remain high. Without lower rates, we think it is going to be difficult to achieve the double-digit earnings growth currently forecasted for 2024. Moreover, profit margins remain high relative to history and have not yet completely erased the overearning experienced during the Covid pandemic. The scenario of strong earnings growth will likely require strong revenue growth rather than higher margins; this is not a likely scenario without lower rates.

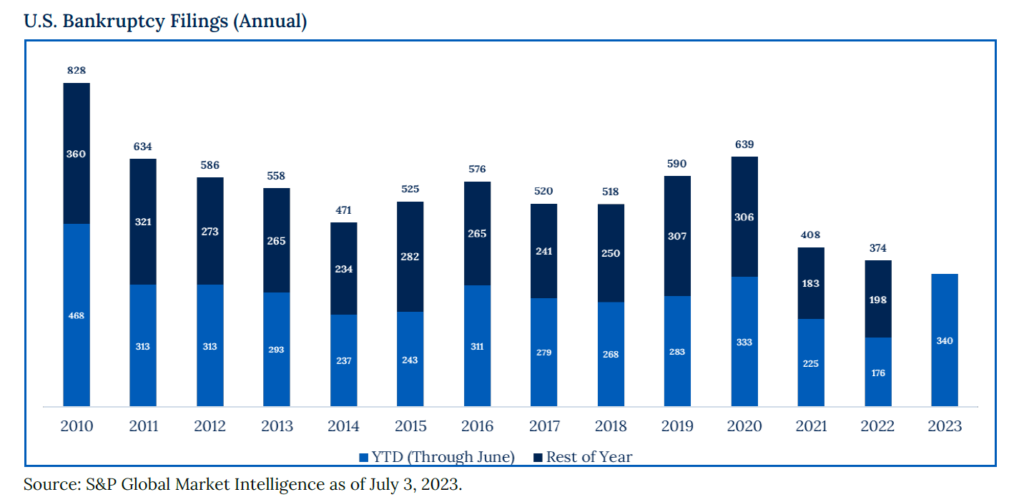

The impact of higher rates has initiated a default cycle, albeit a shallow one thus far. Looming over the horizon are walls of debt maturities in the commercial real estate and corporate debt markets, which grow in 2024 but substantially increase in 2025-27. Will inflation slow fast enough to relieve this pressure driving debt defaults? Is there enough liquidity in the hands of alternative lenders, as the banking sector retreats, to support good borrowers with bad balance sheets even if rates stay high? This collision course in the timeline is one we are watching closely. We expect the liquidity support provided by the Fed and regulators post-SVB to reverse over the rest of 2023. If so, and irrespective of whether defaults rise materially, fresh capital in the private credit markets is being priced at attractive returns and preparing for this early-cycle allocation seems prudent.

There is relative value in Small Caps if the U.S. economy avoids recession. To be clear, Small Caps are much more sensitive than Large Caps to economic growth and, correspondingly, interest rates, and this is why we are underweight. However, for longer-term investors, our capital market assumptions suggest a significantly richer opportunity for this asset class based on relative valuations. There are cyclical and secular drivers in play now versus the pre-Covid environment that could provide support, namely the shortage in housing stock and an apparent policy commitment to infrastructure and re-shoring of manufacturing supply chains. Year-to-date through June, these drivers have led to over 100 basis points of outperformance for the Russell 2000 Index versus the equal-weighted S&P 500 Index. While not a pound-the-table moment, Small Caps look attractive relative to Large.

The Micro (Bottom-up) Picture

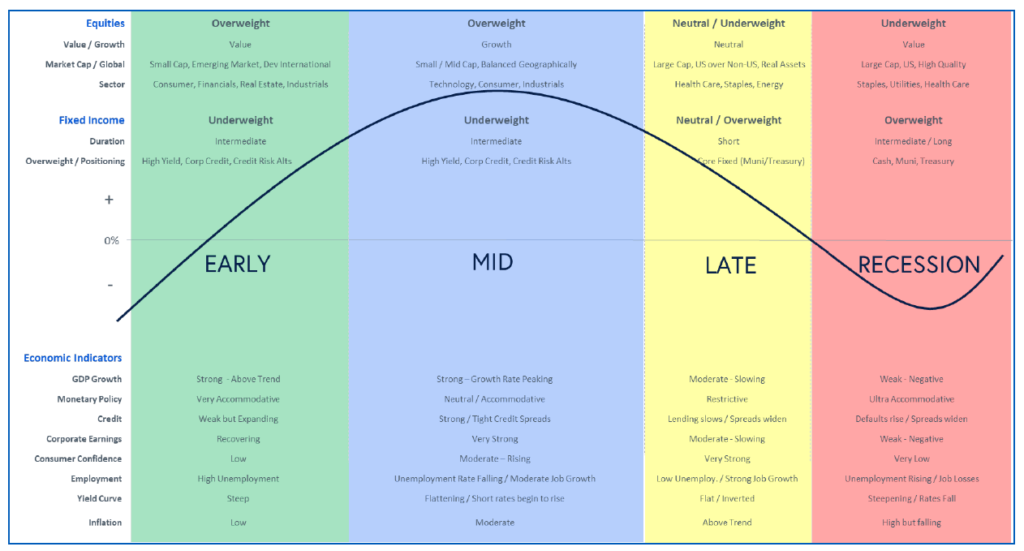

The “thread-the-needle” case, where Fed rate hikes bring down inflation without causing a tough (or even shallow) recession, appears to be the market’s base case. We therefore continue to recommend small tactical adjustments to portfolios to account for our assessment of valuation-driven risk/reward tradeoff, direction of our economic market cycle dashboards, and a general sense of what asset types do better tactically in the current phase of the business cycle.

Valuation primarily keeps us underweight Growth, just as it keeps us overweight Stability. In other words, bond yields should attract capital from equities. However, inside this broad direction are a number of recent shifts outlined in this and prior tactical memos, some of which reflect the classic anticipation of a business cycle inflection:

- Second consecutive increase to Core Fixed Income with the goal of further normalizing duration. Further emphasizing the hedge against falling rates and/or an equity correction.

- Taking advantage of improved outlook for Credit Risk Alternatives by moving back to Strategic target weights.

- Trimming overweight to Equity Risk Alternatives back to neutral versus Strategic targets. Recognizing that it will take time to receive proceeds for LP investors, we are lifting Small Cap U.S. Equities back towards target in anticipation of the end of the interest rate hiking cycle.

- Reducing holdings of Short-duration/Cash to fund extension of duration and Credit Risk Alternatives looking to lock in yields in anticipation of a near-term peak. The remaining short-duration exposure is an offset to the underweight to Growth (“equities”) which we have maintained while the U.S. Market Cycle Dashboards register negative readings.

- Though not a tactical adjustment, a strong recommendation to assess overall liquidity budget for portfolios to allocate to Private Markets, as valuations offer the potential for improved vintage returns.

After a difficult 2022 for financial assets, we expected 2023 to deliver the road back to normal. We just expected it to be bumpier (with all due respect to those in the regional banking sector). Macro risks — for example, geopolitical ones such as U.S./China relations, fiscal ones such as rising U.S. debt service, and the far-from-conquered developed market inflation battle — drive our cautious positioning. However, we are guided and disciplined by the medium- and long-term outlooks embedded in our tools like the Dashboards and Capital Market Assumptions. Indeed, while 2023 is far from over, we have witnessed some market normalization that long-term, goals-oriented investors should cheer. Specifically, the return for each unit of risk in fixed income has increased dramatically. Along the same lines, we think the deconditioning of investors to expect low interest rates is in process, and we are hopeful this lack of low rates suggests better capital allocation across the board for risk assets.

Disclosures

Past Performance Is No Guarantee of Future Performance. Any opinions expressed are current only as of the time made and are subject to change without notice. This report may include estimates, projections or other forward-looking statements, however, due to numerous factors, actual events may differ substantially from those presented. The graphs and tables making up this report have been based on unaudited, third-party data and performance information provided to us by one or more commercial databases. Additionally, please be aware that past performance is not a guide to the future performance of any manager or strategy, and that the performance results and historical information provided displayed herein may have been adversely or favorably impacted by events and economic conditions that will not prevail in the future. Therefore, it should not be inferred that these results are indicative of the future performance of any strategy, index, fund, manager or group of managers. While we believe this information to be reliable, Pathstone bears no responsibility whatsoever for any errors or omissions. Index benchmarks contained in this report are provided so that performance can be compared with the performance of well-known and widely recognized indices. Index results assume the re-investment of all dividends and interest. Moreover, the information provided is not intended to be, and should not be construed as, investment, legal or tax advice. Nothing contained herein should be construed as a recommendation or advice to purchase or sell any security, investment, or portfolio allocation. Any investment advice provided by Pathstone is client specific based on each clients’ risk tolerance and investment objectives. This presentation is not meant as a general guide to investing, or as a source of any specific investment recommendations, and makes no implied or express recommendations concerning the manner in which any client’s accounts should or would be handled, as appropriate investment decisions depend upon the client’s specific investment objectives.

U.S. Large Cap Equity is represented by the S&P 500 Index, with dividends reinvested. U.S. Small Cap Equity is represented by the Russell 2000 Index. Developed Non-U.S. Equity is represented by the MSCI EAFE Index. Emerging Market Equity is represented by the MSCI EM Index. Real Estate is represented by the S&P Global Property Index. Commodities are represented by the Bloomberg Commodity Index. Natural Resource Equities are represented by the S&P North American Natural Resources Index. U.S. High Yield Debt is represented by the Bloomberg Barclays U.S. Corporate High Yield Index. Emerging Market Debt is represented by the JPM GMI-EM Global Diversified Index. U.S. Aggregate Bonds is represented by the Bloomberg Barclays U.S. Aggregate Bond Index. U.S. Treasuries is represented by the Bloomberg Barclays U.S. Treasury Index. U.S. Municipal Bonds is represented by the Bloomberg Barclays Municipal 1-10yr Index.