- Markets continued to rise in February, once again led by U.S. small caps. Breadth has been strong, meaning gains across equities have been widespread, with 92% of S&P 500 companies trading above their 50 day moving average. A big shift from where the market stood at December’s lows, when only 1% of S&P 500 companies were trading above their 50 day moving average.

- U.S. Real GDP increased by 2.9% in Q4; another solid quarter of growth led by consumer spending and business investment. Across the globe, slowing economic activity has been consistent with softening fundamentals. Industrial production within Germany continues to fall and China manufacturing PMI remains below 50, signaling contraction.

- Progress on trade negotiations between the U.S. and China, leading towards a “historic” agreement, has put tariff increases on hold. Brexit uncertainty lingers, as politicians in the UK have been considering allowing an extension to the March 29th deadline. Investor sentiment remains largely optimistic despite the lack of clarity.

- The Fed’s dovish tone has put a hold on further rate decisions for now, and discussions of ending the balance sheet runoff are ongoing. Market expectations for a rate hike this year continue to fall, and investors will look for updated projections for the monetary policy from the Fed after the upcoming meetings on March 19-20th.

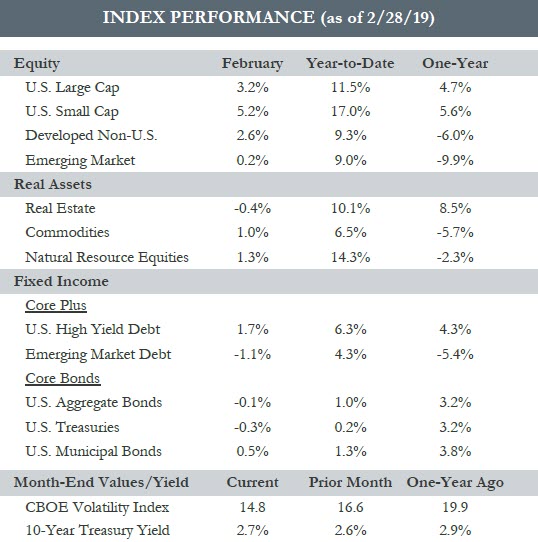

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Please see the full PDF version for important disclosures.