Key Takeaways

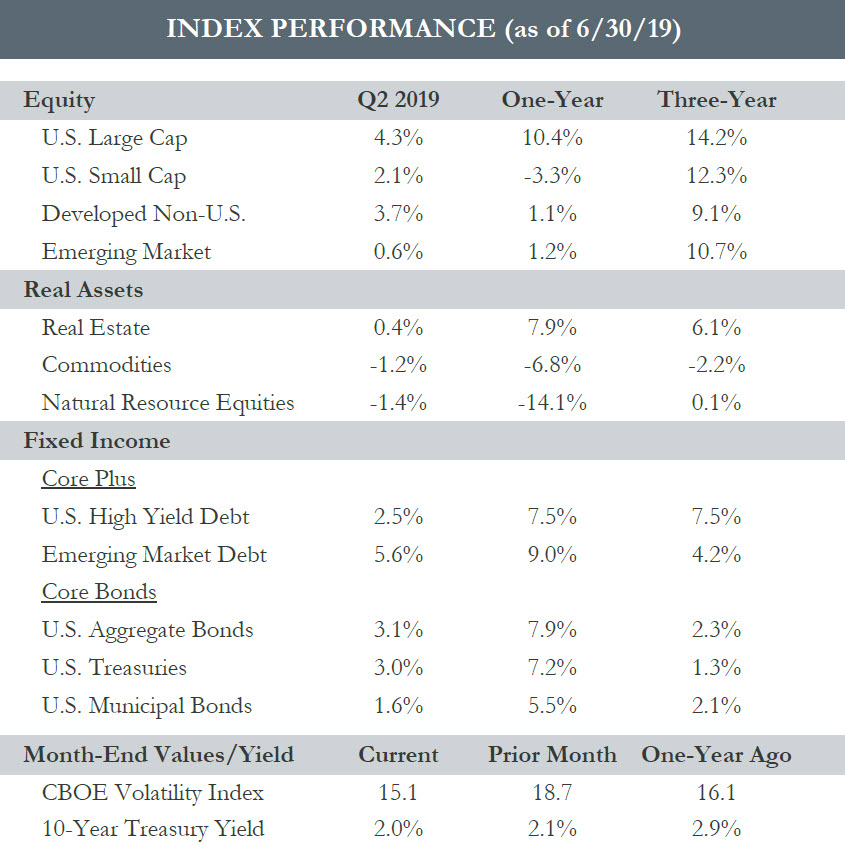

- The second quarter proved to be another period of solid returns, however, the path taken during the three- month period was anything but smooth. Equities advanced in April, fell in May, and rallied in June. The S&P 500 is up over 18% year-to-date—an impressive first half of the year.

- U.S. equities led the way in Q2, besting their international counterparts. Trade sentiment and weaker economic fundamentals outside of the U.S. allowed domestic equities to outperform.

- The bond market once again held the attention of investors through the quarter. Yields fell across the board, driving strong gains in treasuries as Central Banks took a dovish tone. The 10-year Treasury yield dropped by roughly 50 basis points in Q2 to close the quarter at 2.0%, a level last seen in 2016.

- The Fed kept rates unchanged in June, but indications point to a rate cut coming in July. While economic data is consistent with a slower pace of expansion ahead, persistently low inflation, trade uncertainty, and concerns about global growth have led to a more cautious outlook. The ECB also struck a dovish tone and indicated more stimulus could be on the way.

- Trade talks are back on, and additional tariffs are on hold after the G20 Summit in Japan at the end of June. While markets seem to be at ease, real progress on trade negotiations between the U.S. and China leaves something to be desired.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Quarterly Commentary

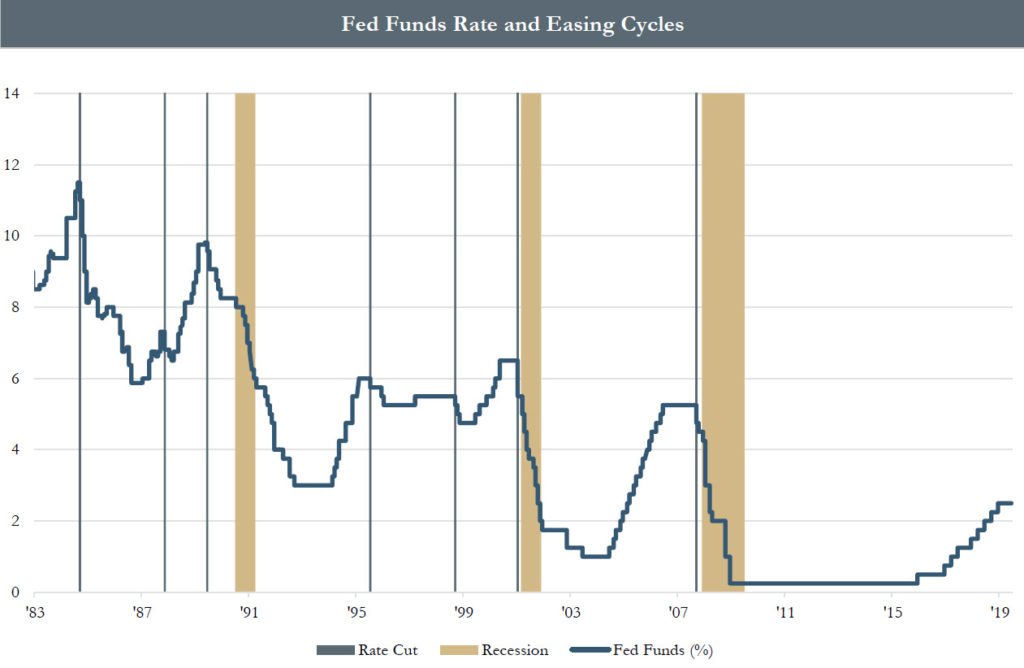

- Major Central Banks have shifted the direction of monetary policy over the last year. After indicating a pause to the tightening cycle to start the year, the Fed took another dovish pivot at the June meeting. Rhetoric from the Fed suggests that they will “act as appropriate to sustain the expansion” as uncertainties about the outlook have increased. The ECB has indicated that a new round of stimulus might be on the way.

- The updated economic projections from the Fed left the median Fed Funds Rate forecast for 2019 unchanged. However, looking deeper into the data there are eight participants expecting lower rates through the end of the year, seven of which by 50 basis points.

- Broadly speaking economic fundamentals remain supportive of the current expansion, though uncertainty over the future outlook has the Fed leaning cautiously. An “insurance” cut seems likely, with markets pricing in a rate cut in July as an almost certainty.

- Questions remain on whether the July cut will be 25 or 50 basis points. The beginning of the last two easing cycles (January 2001 and September 2007) both started with a 50 basis point cut, but economic and credit fundamentals were much weaker when compared to today, and recessions followed soon afterwards. Prior to that, in the mid-1990’s there were two periods of rate cuts and no immediate recession.

- We continue to monitor the communications from Fed officials and the evolving dot plot for indication of the outlook for monetary policy. The next meeting for the Fed is scheduled for July 30-31.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved.

Source — Bloomberg. St. Louis Fed. Using the Federal Funds Target Rate for data up until December 2008. Afterwards we use Federal Funds Target Range - Upper Limit.

Please read important disclosures in the PDF version of this article.