Market Update | Key Takeaways:

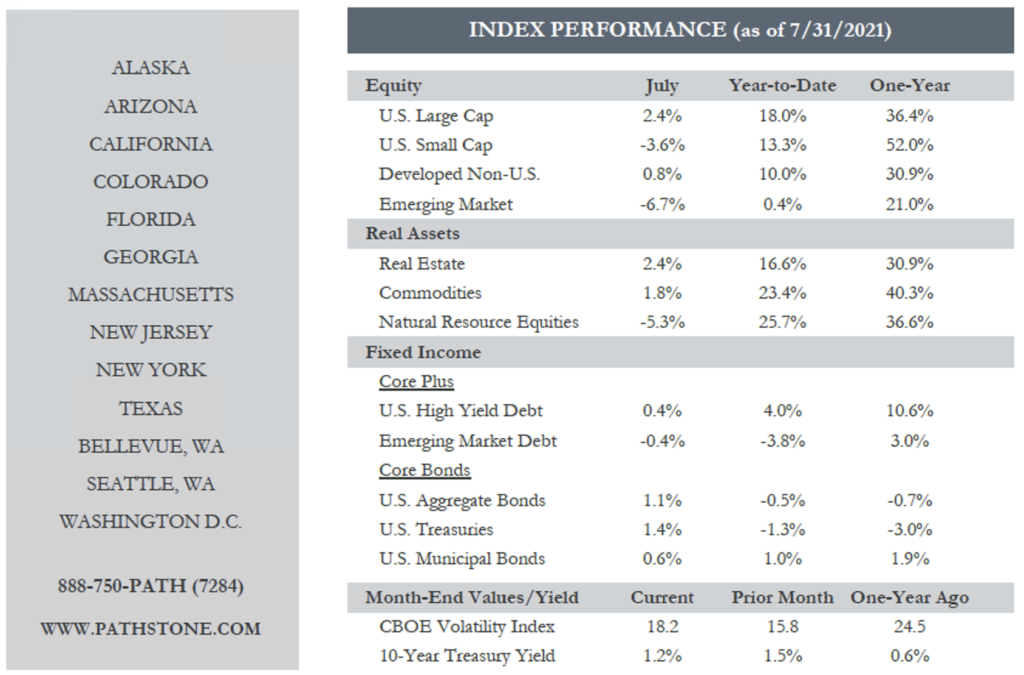

- According to the most recent market update, equities were mixed in July as U.S. Large-Cap Growth buoyed markets while Small Caps, EM Equities, and Natural Resource equities all retreated. Bonds also rallied strongly as the 10-year U.S. Treasury rates dipped below 1.25% as inflation concerns appear to be dismissed by market participants. This marks the fifth month in a row of declining Treasury yields.

- Chinese equity markets sold off as expanding regulatory limitations impact a growing number of companies, causing investors to reconsider risks associated with investing in China. Chinese GDP growth appears to have peaked in Q1 at 18.3% while slowing to a slightly below expectation of 7.9% in Q2.

- U.S. companies continue to report expectation-beating earnings in Q2 but many industries face challenges finding enough employees and rebuilding their inventories as we move into the second half of the year. According to Factset, with 59% of S&P 500 companies reporting as of July 30th, 88% have reported positive revenue and earnings surprises.

- Congress begins its review of the proposed $1 Trillion “Infrastructure Investment and Jobs Act” in the hopes of coming to a bipartisan agreement shortly.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized

Source — Sources: Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.