Key Takeaways

- Headline inflation has cooled off in Q3 with CPI readings of 8.5% and 8.3% YoY for July and August, but still remains stubbornly high. Core inflation had been flat for several months but picked up again in August to 6.3% YoY.

- On the bright side, payrolls have continued to surprise, as the U.S. economy added 526k jobs in July and 315k in August vs. estimates of 235k and 295k. The strong labor market has allowed the Fed to raise the Fed Funds rate to an upper bound of 3.25% after 75 bps hikes in July and September. Markets are currently pricing in another 100 bps of rate increases by the end of the year.

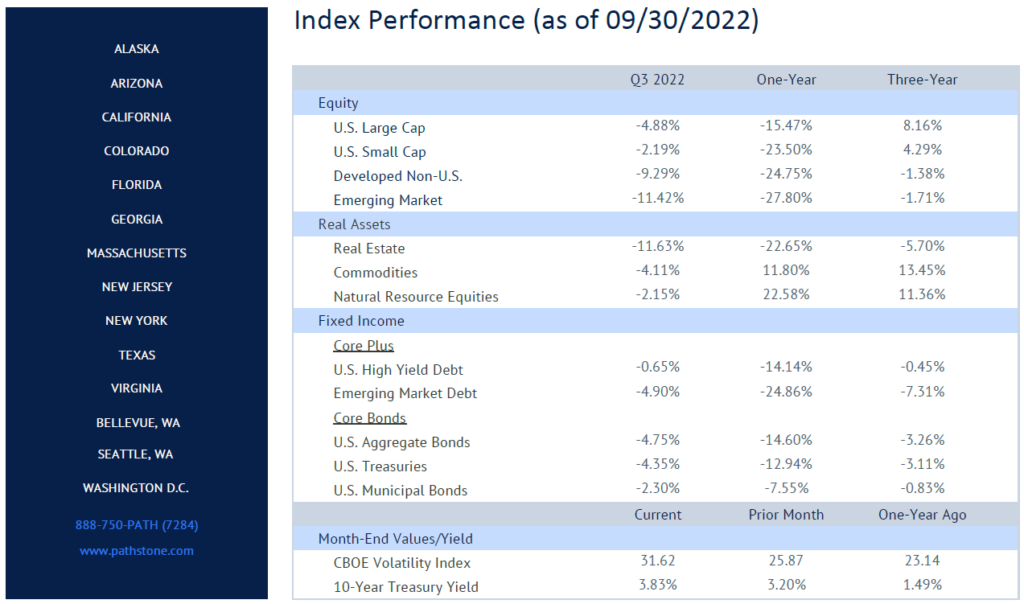

- Q3 was difficult for both equities and bonds and marks the 3rd straight quarter of negative performance for the S&P 500. The large cap index returned -4.9% for the quarter and the NASDAQ dropped -3.9%.

- Investors have taken some risk off the table since the Fed’s meeting at Jackson Hole in August, which provided a clear signal on the Fed’s intent to fight inflation aggressively. Value has outperformed growth and U.S. Large Cap has outperformed U.S. Small Cap since this meeting occurred.

- Developed International equity returns were propelled lower due to weakening currencies vs. the USD. The Euro, Pound, and Yen were down -2.5%, -3.9%, -4.0% in September alone. Chinese equities sold off almost 15% for the month and 22.5% for the quarter as they continue to deal with slower growth hindered by their “Zero-Covid” policies.

- Bonds suffered as 10-year Treasury yields rose over 60 bps and 2-year Treasury yields rose almost 80 bps in September, deepening the inversion of the yield curve.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Quarterly Commentary

- As we enter Q4 of 2022, there is growing concern that the U.S. economy might enter a recession. Our Market Cycle Dashboards havebeen negative for several months now and are at their lowest reading since April 2020.

- Momentum from fiscal and monetary stimulus, as well as economies reopening from the pandemic, is fading, evidenced by weakerconsumption and slowing manufacturing. Higher mortgage rates, combined with a stronger dollar, will present a challenge to economicgrowth in the months to come.

- Neither the Fed nor the Federal government are likely to spur growth if inflation continues to be hotter than expected. This will meanhigher interest rates for the foreseeable future, negatively impacting the return prospects for long-duration assets such as longer maturity bonds and growth equities.

- There is good news in the U.S. labor market, which has been resilient thus far, with persistent strength in the number of jobs added everymonth and no weakness in weekly initial jobless claims. The bad news is that this labor strength is a principal reason for stubborn inflation and will be a key barometer for the duration of the Fed’s tough stance.

- Higher interest rates have revealed cracks in not only the U.S. economy, but the global economy as well. The Bank of England has alreadyhad to reverse course and buy treasuries to support UK pensions searching for liquidity. If a recession hits global economies, there couldbe other unforeseen consequences.

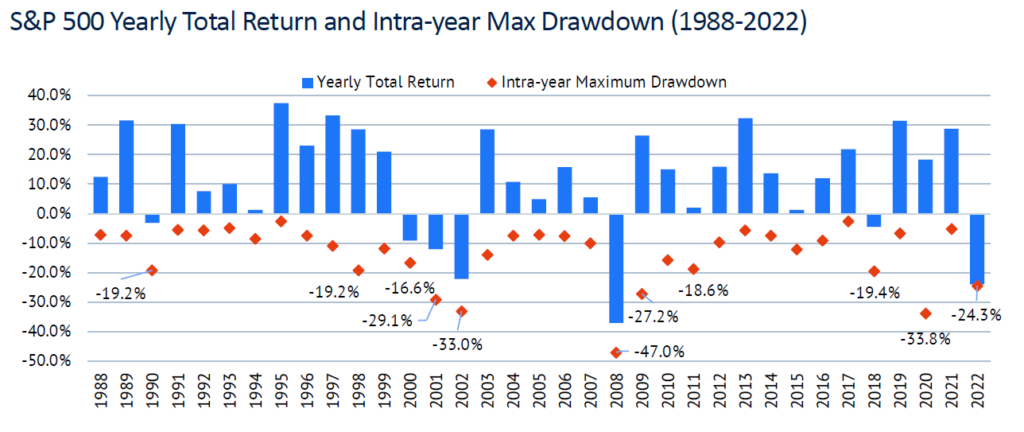

- For most investors, 2022 has been a difficult year, most clearly viewed by the performance of a traditional 60/40 portfolio – down 21%.A lingering pandemic, war, inflation, and interest rates have created a pessimistic outlook for Q4. Volatility is likely to remain elevatedand the current environment calls for a disciplined approach. Periodic rebalancing at attractive valuations and being broadly diversifiedwith an overweight to short-duration fixed income are our most powerful tools at this time.

You cannot invest directly in an index; therefore, performance returns do not reflect any management fees. Returns of the indices include the reinvestment of all dividends and income, as reported by the commercial databases involved. Returns over one year have been annualized.

Source — Bloomberg, Morningstar, treasury.gov. S&P Dow Jones Indices.

Please see PDF for important disclosures.